Deposit risk is a form of liquidity risk faced by financial institutions. It arises because banks rely heavily on customer deposits, whether these are time-bound deposits with fixed maturity dates or flexible deposits that customers can withdraw at any moment. Since deposits are a major source of funding for banks, sudden or unexpected withdrawals can strain a bank’s liquidity, challenging its ability to meet obligations. Unlike other risks, deposit risk is driven primarily by the behavior and confidence of depositors.

Types of Deposit Risk

Deposit risk can take several forms, each tied to how depositors interact with their accounts. The main categories are early withdrawal risk, rollover risk, and run risk.

Early withdrawal risk occurs with time deposits—such as certificates of deposit or term deposits—when a depositor decides to pull out funds before the agreed maturity date. This may be allowed under the terms of the contract or dictated by regulations in some regions. Although banks often impose penalties for early withdrawals, such actions still disrupt liquidity planning and create uncertainty about future cash flows.

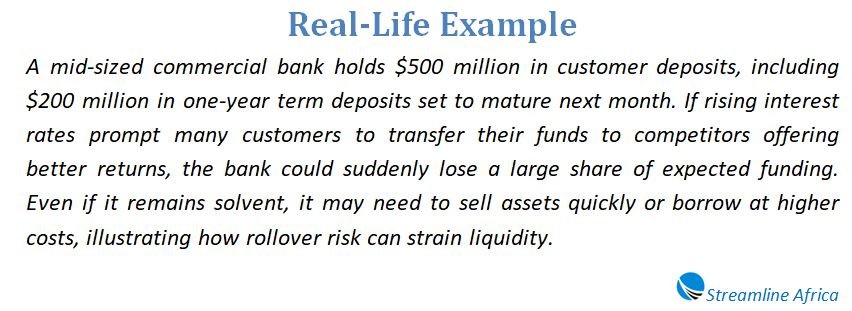

Rollover risk is associated with time deposits that are about to mature. When customers choose not to reinvest or “roll over” their deposits, banks lose a portion of expected funding. The decision not to roll over can stem from better interest rate offers elsewhere, a decline in the bank’s creditworthiness, or personal financial needs of the depositor.

Run risk is most relevant for demand deposits, such as savings or checking accounts, where funds can be withdrawn at any time. If many customers simultaneously lose trust in a bank—perhaps fearing insolvency—a bank run may occur. In this scenario, the withdrawal pattern resembles a combination of early withdrawal and rollover risks, but on a potentially massive scale. Bank runs, even when sparked by rumors, can quickly destabilize institutions and sometimes the broader financial system.

The Link to Refinancing Risk

When depositors withdraw funds and a bank cannot replace them with new deposits, the institution faces the possibility of a liquidity shortfall. If the bank also struggles to borrow from other sources to cover these withdrawals, it experiences refinancing risk. This creates a dangerous cycle: without access to new funding, the bank may be unable to meet its obligations, which can further erode depositor confidence and worsen the problem.

Measuring Exposure to Deposit Risk

Understanding how exposed a bank is to deposit risk requires careful measurement. For early withdrawal risk, exposure is the total amount of balances in time deposits that are not due on a given date. In other words, these are funds that could potentially be withdrawn prematurely, creating unexpected cash outflows.

Rollover risk exposure corresponds to the total value of time deposits that are maturing on a particular date. If a significant share of depositors declines to reinvest, the bank must find alternative funding sources to replace these maturing deposits.

Run risk exposure is measured by the sum of all balances in non-maturity deposit accounts, such as demand deposits, on a given date. These accounts represent an ever-present risk since funds can be withdrawn at any time.

Interconnection of Risks

These risks are not isolated. Early withdrawal reduces the amount of cash flows that banks expect in the future, which in turn amplifies rollover risk. The relationship between maturity and risk is also notable: deposits with longer maturities carry greater early withdrawal risk because of the longer time frame over which depositors may change their minds, yet they tend to have lower rollover risk since depositors are locked in for a longer period. Conversely, short-term deposits present less early withdrawal risk but higher rollover risk since depositors must decide whether to renew more frequently.

Factors Influencing Deposit Behavior

Several factors influence whether depositors choose to withdraw funds early, roll over deposits, or participate in runs. Interest rates play a critical role: if competitors offer higher returns, depositors may move their funds. Similarly, a bank’s credit rating signals its stability, affecting depositor confidence. Deposit insurance is another key determinant, since insured funds reduce the incentive for depositors to withdraw quickly at the first sign of trouble. The size of a deposit and its age also matter—larger deposits or newer accounts may be more sensitive to changes in market conditions.

Conclusion

Deposit risk highlights the vulnerability of financial institutions to depositor behavior. While penalties, insurance schemes, and careful liquidity management can reduce exposure, no bank is entirely immune. By monitoring depositor tendencies, market conditions, and their own financial health, banks can better prepare for potential outflows. For depositors, understanding these risks underscores why institutions place such emphasis on confidence and stability—the trust of account holders is, after all, the backbone of modern banking.

Frequently Asked Questions deposit Risk

How does deposit risk connect to liquidity?

Since deposits are a bank’s main funding source, sudden outflows can drain available cash, forcing the bank to borrow or sell assets quickly.

What are the main types of deposit risk?

The three primary forms are early withdrawal risk, rollover risk, and run risk—each tied to how and when depositors take back their money.

Why is early withdrawal a concern for banks?

Even with penalties, early withdrawals create unpredictable cash outflows, making it harder for banks to plan liquidity needs.

What triggers rollover risk?

When time deposits mature, customers may choose not to renew, often because of better rates elsewhere or doubts about the bank’s stability.

What causes a bank run?

Run risk happens when many depositors, fearing a bank’s failure, withdraw funds at the same time, amplifying liquidity pressure.

What factors shape depositor behavior?

Interest rates, deposit insurance, the bank’s credit rating, and even the size and age of deposits all influence withdrawal and rollover decisions.