When companies pursue mergers or acquisitions, one of the clearest and most straightforward ways to complete the deal is through an all-cash, all-stock offer. This structure may sound complicated at first glance, but the concept is quite simple: one company proposes to buy every outstanding share of another company and pays shareholders entirely in cash. While this type of offer can seem attractive because of the immediate payout, there are layers of strategy, finance, and risk behind the scenes that shape how these deals unfold.

This guide explores how all-cash offers work, why some companies choose them, the advantages they provide to shareholders and buyers, and the potential limitations that can complicate the process.

What an All-Cash, All-Stock Offer Means

In an all-cash, all-stock offer, the acquiring company proposes to purchase every share of the target company using cash as the only form of payment. Unlike stock-swap deals, where shareholders receive new shares in the acquiring company, an all-cash deal gives the sellers immediate liquidity. To encourage shareholders to accept the proposal, the acquiring company typically offers to pay more than the stock’s current market value. This premium acts as an incentive, especially for investors who may be unsure about the long-term direction of the company being acquired.

Shareholders benefit from the immediate financial gain, but they also give up their ownership stake in the company. For some, the certainty of cash is appealing; for others, especially long-term investors, selling may not always feel like the ideal scenario. Still, these offers remain a common method for completing takeovers, especially when acquirers want full control without diluting their own share base.

Why Companies Make All-Cash Offers

Companies choose all-cash transactions for several strategic reasons. First, cash is seen as a strong signal of confidence. When a buyer is willing to spend billions in cash to acquire a business, it communicates certainty about the future value they expect to extract from the deal. Investors often interpret this as a sign that the acquiring company is financially healthy and expects substantial returns from the combined operation.

Second, all-cash deals avoid the complications that arise when issuing new shares. When companies use stock to fund acquisitions, they must consider share dilution, valuation disagreements, and how the additional shares may influence voting control. By paying cash, the buyer sidesteps these issues and completes the transaction with cleaner ownership lines.

Third, companies may opt for cash when speed is important. Stock-for-stock transactions often involve deeper regulatory review or require shareholder votes. Cash deals, on the other hand, can sometimes move faster because they rely on direct payment rather than restructuring share ownership.

How Shareholders Benefit from All-Cash Deals

For shareholders of the target company, the primary benefit is the immediate premium they receive over the existing stock price. When news of a cash offer breaks, the stock often rises sharply, reflecting investor expectations that the transaction will close at the offered price.

If analysts and investors believe the merged business will be stronger and more profitable, the stock market may respond with optimism—even before the deal is finalized. Cost savings, operational efficiencies, and combined expertise often contribute to this confidence. For example, if the acquiring company plans to streamline redundant operations or integrate technologies that reduce long-term expenses, those improvements may ultimately increase the value of the combined firm.

Shareholders of companies with uncertain futures may also welcome a cash buyout. If the target company’s stock has been underperforming or facing market pressures, an all-cash offer at a premium may represent a strong exit opportunity. Selling at a guaranteed price can feel more secure than riding out volatility or waiting for a potential turnaround.

How Buyers Finance All-Cash Acquisitions

Not every acquirer has enough money readily available to purchase another company outright. As a result, buyers often rely on a mix of funding sources to gather the capital required.

Issuing Bonds or Equity

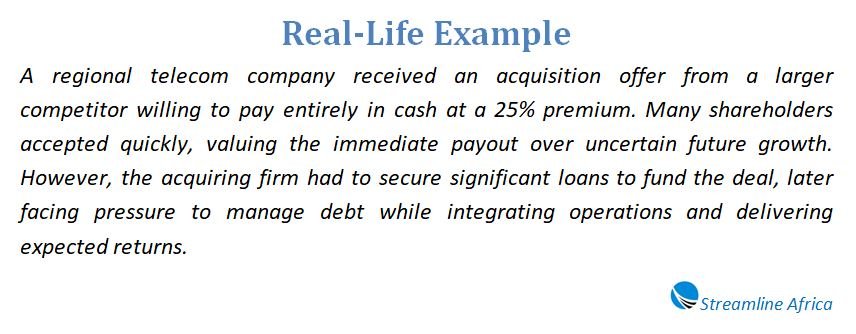

One route is to issue new bonds. This allows the acquiring company to borrow large sums from investors, promising to repay the principal at maturity along with periodic interest payments. Bonds provide flexibility since the company can spread repayment over many years. However, taking on debt adds pressure to future cash flows, and if economic conditions shift, the interest burden may become more difficult to manage.

Another option is raising funds by issuing new stock. A privately held company might launch an initial public offering to generate cash, while public companies sometimes issue additional shares. Although this can provide significant capital, it risks diluting ownership for existing shareholders.

Taking Out Large Loans

Loans from financial institutions represent another pathway. Banks may partner to provide syndicated loans for particularly large acquisitions. However, high interest rates or unfavorable borrowing terms can make this approach expensive. Heavy borrowing might also affect the newly combined company’s financial flexibility, potentially limiting future growth investments or making further borrowing more difficult.

Key Challenges and Complications of All-Cash Deals

While all-cash offers are often viewed as simple and decisive, they come with several challenges that both buyers and sellers must consider.

Currency and Exchange Rate Risks

When either company operates internationally, the transaction may involve multiple currencies. Because exchange rates change constantly, the final amount paid can shift if the deal is delayed. A small fluctuation in currency value can significantly alter the purchase price, especially in billion-dollar transactions. To protect themselves, companies sometimes use hedging tools, but those strategies come with added costs.

Tax Consequences for Shareholders

For shareholders, receiving cash triggers a taxable event. If the price they receive is higher than their purchase price, the profit becomes a capital gain, which may reduce the overall benefit. Even though these tax obligations are similar to a normal stock sale, the forced timing of the transaction can be inconvenient for investors who prefer to manage their investments strategically.

Strain on the Acquirer’s Finances

Issuing bonds or taking on large loans increases the acquiring company’s debt load. If revenues decline or interest rates rise unexpectedly, debt payments may strain the business. This financial pressure can slow innovation, limit expansion, or reduce the company’s ability to react quickly to market conditions.

Companies that overextend themselves during acquisitions run the risk of weakening their financial stability, which can ultimately undermine the value they hoped to gain from the purchase.

Alternatives to All-Cash, All-Stock Offers

Many acquisitions do not rely entirely on cash. Alternatives include:

Stock-for-Stock Transactions

Instead of cash, shareholders receive new shares from the acquiring company. These deals typically avoid immediate tax consequences because no cash is changing hands. They also allow shareholders to retain an ownership stake in the newly merged company, which may appeal to long-term investors.

Hybrid Deals

Some acquisitions combine cash with newly issued shares. This approach balances the immediacy of cash with the long-term participation offered by stock. It also allows buyers to reduce the amount of debt needed to complete the acquisition.

These alternatives provide flexibility and may be better suited to companies trying to manage tax considerations, balance sheets, or strategic interests.

Final Thoughts

An all-cash, all-stock offer represents a direct and often appealing method of executing an acquisition. Shareholders benefit from a guaranteed premium, while acquirers gain full control of the target company without complications that arise from issuing new shares. However, the structure is not without drawbacks. Tax obligations, exchange rate fluctuations, and the potential debt burden can all influence the success of the transaction.

Companies must carefully evaluate their financial capacity, market conditions, and long-term strategic plans before choosing this type of acquisition. Likewise, shareholders should consider their investment goals and tax situation when deciding whether to support such a proposal.

All-cash offers remain an important tool in the world of mergers and acquisitions, but they work best when paired with thoughtful planning, clear financial strategy, and a full understanding of the risks involved.