Public utilities operate within a unique financial environment shaped by regulation, long-term infrastructure needs, and unpredictable operating costs. To keep services reliable and affordable, regulators allow these companies to treat certain expenses differently from ordinary businesses. One of the most important tools for achieving this is the concept of regulatory assets. These assets enable utilities to postpone the immediate financial impact of specific expenses and recover those costs over time through customer rates. Understanding how these assets work is essential for grasping the financial structure of regulated industries such as electricity, water, and natural gas.

A regulatory asset may not be a physical item like a power line or a water treatment tank. Instead, it represents costs the utility has already incurred but is permitted to treat as long-term recoverable amounts rather than recognizing them as expenses right away. This accounting treatment helps prevent sudden spikes in utility bills and keeps financial reporting in line with the long-term nature of public infrastructure investments.

What Regulatory Assets Represent in Utility Accounting

In the simplest terms, a regulatory asset arises when a public utility spends money today but is approved by regulators to recover that expense from customers in the future. Instead of reducing profits immediately by recording the cost on the income statement, the utility places it on the balance sheet as an asset. This is done only when a regulatory authority confirms that the cost is legitimate and will be included in future rate-setting.

Expenses that commonly qualify as regulatory assets include environmental compliance projects, repairs after major storms, energy procurement costs, and expenses tied to long-term infrastructure improvements. Because utilities must respond quickly to emergencies or comply with environmental standards, these costs can be substantial and unpredictable. Allowing them to be deferred provides stability both for customers and the company.

This treatment recognizes an important reality: utilities operate under a regulated rate structure that is designed to ensure they earn a fair return while providing essential services. A regulatory asset reflects a promise that the utility will eventually recover its costs when customer rates are adjusted.

How Regulatory Rules Shape the Recording of These Assets

The accounting for regulatory assets is governed by standards designed specifically for public-sector and regulated entities. In the United States, the Governmental Accounting Standards Board (GASB) establishes these rules. GASB Statement No. 62 is the key guideline that outlines how and when utilities can defer costs as regulatory assets.

Under this standard, utilities must meet specific criteria before they can classify a cost as a regulatory asset. First, the cost must be directly tied to providing regulated services. Second, regulators must approve the cost for future rate recovery. Third, the utility must be able to reasonably estimate the period over which the cost will be recovered.

GASB 62 covers a wide range of possible expenses. These include cleanup and decommissioning costs for old plants, losses from retiring outdated equipment, power supply expenses during unusual price spikes, repairs after severe weather events, and certain financing costs. Some of these expenses occur suddenly and unpredictably, while others arise from long-term operational or environmental obligations.

In addition, utilities must follow strict documentation practices to track how each regulatory asset will be recovered. This includes amortization schedules, details of regulatory decisions, and explanations of the costs included. All of this information must be disclosed clearly in the utility’s financial statements, giving investors and customers transparency about future rate impacts.

Why Regulatory Assets Matter to Utilities and Their Stakeholders

Regulatory assets serve a practical purpose: they help match revenues and expenses in a way that reflects the long-term timeline of utility operations. Because public utilities operate large networks of essential infrastructure, their financial performance cannot be evaluated in the same way as private non-regulated companies. Recognizing costs immediately could result in erratic financial results and unpredictable rate changes for customers.

Instead, regulatory assets act as a financial bridge, allowing utilities to recognize the cost over several years as they collect revenue through customer rates. This creates a smoother financial trajectory and helps regulators avoid sudden spikes in electricity, water, or gas bills. Customers still ultimately pay for the approved cost, but the burden is spread across time rather than concentrated in a single billing period.

Utilities benefit from this approach because it stabilizes cash flows, supports credit ratings, and maintains investor confidence. Meanwhile, regulators maintain oversight to ensure that deferred costs are legitimate and that customers are protected from unnecessary charges. This balance between financial health and public interest is at the heart of regulated utility accounting.

How Regulatory Assets Affect Financial Statements

When a utility records a regulatory asset, it shifts a cost from an immediate expense to a long-term receivable. Instead of reducing profit in the year the cost occurs, the utility places the amount on its balance sheet. Over time, the cost is gradually amortized, meaning it is expensed in small portions as customers pay the approved rates.

This method allows the utility’s income statement to reflect a more accurate picture of ongoing operations. Without regulatory assets, a single storm or equipment failure could dramatically distort annual financial results. With regulatory accounting, these events are incorporated into long-term planning and rate-setting processes.

From a financial analysis standpoint, regulatory assets often signal large commitments related to infrastructure, compliance, or emergency response. Analysts review disclosures to understand the nature of these assets, their recovery periods, and the regulatory environment that governs them. Changes in regulatory policy, economic conditions, or utility performance may affect whether these assets are recoverable in the future.

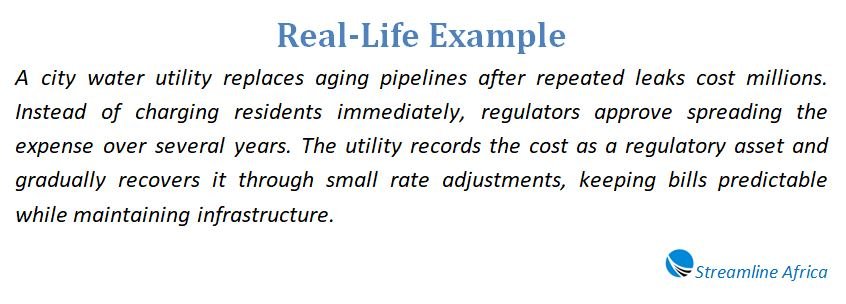

Real-World Illustration: How Utilities Use Regulatory Assets

A clear example of regulatory assets in practice can be seen in major electric utilities across the United States. Large companies often accumulate substantial deferred costs because they manage complex systems exposed to natural disasters, environmental regulations, and long-term infrastructure needs.

For instance, Southern California Edison (SCE), one of the largest electric utilities in the western United States, routinely reports significant regulatory assets in its filings. At the end of a recent fiscal year, the company disclosed billions of dollars in deferred amounts tied to wildfire risk mitigation, grid modernization, environmental compliance, and other regulatory-approved programs. Each of these items represents a cost that regulators have agreed can be recovered through future rates.

The utility must disclose the details of each regulatory asset in the notes to its financial statements. These disclosures include the nature of the costs, the expected recovery timeline, and any assumptions used to calculate amortization. This transparency helps investors gauge the stability of future revenue and the financial health of the company.

Such examples highlight how regulatory assets are intertwined with the long-term responsibilities utilities carry. They ensure that companies can continue investing in safe, reliable service without overwhelming customers with immediate charges.

Read Also: Core Assets vs Non-Core Assets: A Complete Guide to Business Survival and Long-Term Growth

The Role of Regulators in Approving and Monitoring These Assets

Regulatory bodies play a decisive role in determining which costs qualify as regulatory assets. Their decisions directly influence a utility’s financial performance and its ability to recover costs. Regulators assess whether the expense was necessary, prudent, and beneficial to the public. If the regulator determines that customers should not be responsible for a particular cost, the utility must treat the expense as an immediate loss rather than a deferrable asset.

Because these decisions impact both customers and investors, regulators must balance fairness, affordability, and financial stability. This oversight ensures that utilities remain accountable and that deferred costs do not become a mechanism for inflating future rates.

Regulators also require utilities to periodically update their filings, provide documentation, and justify recovery periods. The rigor of this process helps maintain transparency in rate-setting and ensures that customers understand why future bills may reflect past events.

Why Transparency Is Essential in Reporting Regulatory Assets

Given the complexity of these assets and their long-term implications, clarity in financial reporting is crucial. Utilities must show exactly which costs have been deferred, how they will be recovered, and how long recovery will take. This information is important not only for regulators and investors but also for customers who may eventually bear the cost through their utility bills.

Well-maintained disclosures also help avoid misunderstandings and promote trust. If a utility suddenly changes its estimates or if regulators revise their decisions, stakeholders can quickly trace the financial impact by reviewing the detailed notes in the financial statements.

Good transparency supports better governance, more stable financing, and informed decision-making across the organization.

Conclusion

Regulatory assets play a vital role in how public utilities manage major expenses while maintaining affordable and stable rates. By allowing certain costs to be deferred and recovered gradually, regulatory accounting reflects the long-term nature of utility operations. These assets ensure that unexpected events, environmental compliance requirements, and infrastructure investments do not create sudden financial shocks for either the company or its customers.

Regulators, accounting standards, and financial disclosures all work together to ensure these assets are used responsibly and transparently. Real-world examples from major utility companies illustrate how regulatory assets help balance financial stability with public service obligations.

Understanding how these assets work helps clarify why utility bills, regulatory decisions, and financial reports are structured the way they are—anchoring the long-term sustainability of essential public services.

Regulatory Assets – FAQs

Why do utilities use regulatory assets?

They use them to avoid sudden financial losses and to keep customer rates stable over long periods, especially after large or unexpected expenses.

Who decides whether a cost qualifies as a regulatory asset?

Regulatory commissions make that decision. They review the cost and determine if it is appropriate for future recovery.

How do regulatory assets benefit customers?

By spreading recovery over time, customers avoid sudden bill increases after storms, environmental emergencies, or major repairs.

Why are these assets placed on the balance sheet instead of the income statement?

They are deferred because regulators guarantee future recovery. This shifts the cost from a current-period expense to a long-term recoverable asset.

What types of costs usually qualify as regulatory assets?

Storm damage, environmental compliance, power procurement cost spikes, decommissioning obligations, and losses from plant retirements often qualify.

How are regulatory assets amortized?

Utilities expense these deferred amounts gradually over a regulator-approved timeline as customers pay rates that include recovery.

What happens if regulators deny cost recovery?

The utility must immediately expense the cost, which can hurt profit, affect creditworthiness, and impact operational plans.

Why is transparency important when utilities report regulatory assets?

These costs impact future rates, so customers, investors, and regulators need to clearly understand what they are and how long recovery will take.

How do regulatory assets affect financial stability?

They prevent volatility in yearly financial results and help utilities maintain predictable revenue, which is essential for funding infrastructure.

Do all utilities account for regulatory assets the same way?

The exact rules vary by jurisdiction, but most regulated utilities follow GASB or FASB guidance, depending on whether they are public or private entities.

Can regulatory assets ever be written off?

Yes. If recovery becomes unlikely—say due to policy changes or shifting regulatory views—the asset may be impaired or written off.