A Taxpayer Identification Number, commonly called a TIN, is a unique reference assigned to individuals and entities for tax administration purposes in Ghana. It allows the state to accurately identify taxpayers, track compliance, and manage tax records across different institutions. The legal foundation for the TIN system is found in Sections 10 to 12 of the Revenue Administration Act, 2016 (Act 915), which empowers the Commissioner-General of the Ghana Revenue Authority to establish and manage a national taxpayer identification framework. Over time, this framework has evolved to align with Ghana’s broader digital identity reforms, particularly for individual taxpayers.

The Shift to the Ghana Card PIN for Individuals

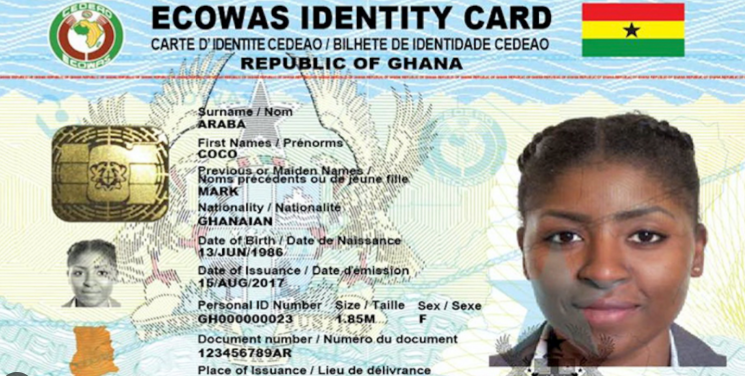

From 1 April 2021, Ghana introduced a significant reform in taxpayer identification for individuals. Instead of maintaining a separate TIN issued solely by the tax authority, the Personal Identification Number (PIN) on the Ghana Card became the official tax identifier for all individual taxpayers. This change applies strictly to natural persons and does not extend to companies or other legal entities.

The reform was designed to reduce duplication, simplify identification, and improve data accuracy across government systems. By linking tax identification to the national biometric identity system managed by the National Identification Authority, the government strengthened its ability to verify identities, prevent fraud, and enhance compliance monitoring. In practical terms, this means that any individual who previously had a GRA-issued TIN now uses their Ghana Card PIN for all tax-related and legally mandated transactions.

Situations Where the Ghana Card PIN Is Required

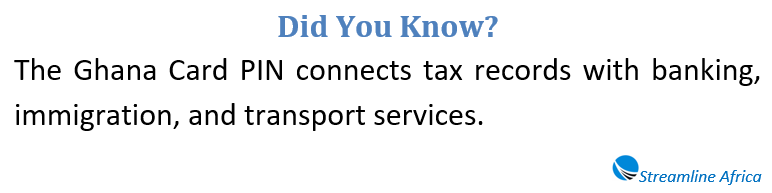

The Ghana Card PIN now serves as a universal substitute for the individual TIN in a wide range of official and commercial interactions. Anytime a process requires an individual’s tax identification, the Ghana Card PIN must be provided. This applies to direct dealings with the Ghana Revenue Authority, such as filing tax returns, registering for tax types, or resolving compliance issues.

Beyond tax administration, the PIN is required when registering a business at the Registrar-General’s Department, opening a bank account, or accessing formal financial services. It is also necessary for registering motor vehicles, applying for or renewing a Ghanaian passport, acquiring or transferring land interests, clearing goods at ports and airports, and obtaining or renewing a driver’s licence. These requirements reflect the government’s policy of using a single, reliable identifier across multiple sectors to improve efficiency and accountability.

How Individuals Obtain and Use Their TIN

For individuals, the process of obtaining a TIN is now inseparable from Ghana Card registration. Any person who needs to meet tax obligations must first register with the National Identification Authority to receive a Ghana Card. Once issued, the Ghana Card PIN automatically becomes the individual’s tax identification number, with no additional application required at the GRA.

To support individuals who previously had a TIN but did not yet possess a Ghana Card, the NIA has been co-located at selected Domestic Tax Revenue Division offices across the country. These centres allow taxpayers to complete Ghana Card registration conveniently within tax service locations. This arrangement ensures continuity for individuals transitioning from the old TIN system while maintaining access to tax services nationwide, including regional capitals and major commercial centres.

TIN Registration for Companies and Other Organisations

While individuals now rely on the Ghana Card PIN, the TIN system remains fully in place for organisations. Companies, partnerships, and other legal persons are still required to obtain and use a TIN issued by the Ghana Revenue Authority. This organisational TIN serves as the primary identifier for all tax obligations, filings, and correspondence with the GRA.

An organisational TIN is mandatory for any business entity that is liable to pay taxes in Ghana. It is also widely used for identification in regulatory, banking, and contractual contexts. Importantly, an organisation can only apply for a TIN after completing registration with the Registrar-General’s Department, since legal incorporation or business name registration establishes the entity’s formal existence.

One-Stop TIN Services at the Registrar-General’s Department

To streamline the business registration process, the GRA has co-located its TIN Centre at the premises of the Registrar-General’s Department. This one-stop arrangement allows directors, shareholders, partners, and board members to complete organisational TIN registration as part of the overall business setup process.

By issuing the organisational TIN alongside incorporation documentation, the system reduces delays and ensures that newly registered businesses can immediately meet their tax obligations. This integration supports ease of doing business, particularly for startups and small enterprises that benefit from fewer administrative hurdles during early operations.

Organisations Exempt from Registrar-General Registration

Not all entities operating in Ghana are required to register with the Registrar-General’s Department. Public sector bodies and special-purpose organisations such as ministries, departments and agencies, metropolitan and district assemblies, public institutions, foreign missions, cooperatives, and trusts fall outside the standard RGD registration framework.

These organisations are still required to obtain an organisational TIN for tax identification and reporting purposes. To do so, they must submit a completed organisational TIN application form together with an introductory letter and any supporting documents specified by the Taxpayer Identification Unit. Applications are processed at designated GRA Taxpayer Service Centres, and once approved, the TIN is communicated to the organisation through official channels, typically via SMS notification.

Categories of Organisations Required to Register

For entities that fall under the Registrar-General’s Department’s jurisdiction, organisational TIN registration applies to a wide range of legal structures. These include sole proprietorships operating under registered business names, companies limited by shares, companies limited by guarantee, partnerships, external or foreign companies, and subsidiary business names linked to existing companies. Each of these entities must maintain a valid TIN for all tax-related activities throughout their operational life.

Verifying TINs and Ghana Card PINs

Verification plays an important role in maintaining trust and accuracy within the tax system. Ghana provides an official online portal that allows users to confirm the validity of an organisational TIN or an individual’s Ghana Card PIN when it is presented for official or commercial purposes. This service is particularly useful for banks, employers, contractors, and institutions that are legally required to confirm taxpayer identity before completing transactions.

Verification helps reduce impersonation, incorrect data entry, and compliance risks, ensuring that records across institutions align with the national taxpayer database.

Continued Use of Existing Organisational TINs

It is important to note that companies, corporations, and other legal persons must continue using their existing organisational TINs. The introduction of the Ghana Card PIN does not replace organisational TINs and has no impact on how entities file returns, pay taxes, or interact with the Ghana Revenue Authority. The reform applies strictly to individual taxpayers.

Special TIN Registration for Mandated Institutions

To support compliance by institutions legally required to collect TINs from their clients, the GRA has introduced special registration arrangements. Mandated institutions listed under the Revenue Administration Act are permitted to submit completed TIN application forms on behalf of their customers through a dedicated service email managed by the Taxpayer Identification Unit.

Under this arrangement, the GRA processes the submitted forms, generates the TIN, and communicates it back to the institution for onward delivery to the client. This approach simplifies access to TINs for individuals and organisations conducting transactions through regulated intermediaries. While currently limited to selected institutions, ongoing discussions aim to extend this facility across the financial and regulatory sectors to further improve taxpayer convenience and compliance.

FAQs

Why Was the Ghana Card PIN Introduced as a Replacement for Individual TINs?

The Ghana Card PIN replaced individual TINs to reduce duplication, improve data accuracy, and create a single national identity number that works across tax, banking, and other public services.

Who Uses the Ghana Card PIN as a TIN?

Only individual taxpayers use the Ghana Card PIN as their TIN. This applies to all natural persons earning income or engaging in transactions that require tax identification.

Do Companies Still Need a Separate TIN?

Yes, companies and other legal entities must continue using the organisational TIN issued by the Ghana Revenue Authority. The Ghana Card PIN does not apply to businesses.

What Transactions Require the Ghana Card PIN?

It is required for tax filing, business registration, opening bank accounts, passport applications, vehicle registration, land registration, clearing goods at ports, and obtaining a driver’s licence.

How Does an Individual Get a TIN Today?

An individual gets a TIN automatically by registering for the Ghana Card. Once issued, the Ghana Card PIN becomes the person’s official tax identification number.

Can Organisations Register for a TIN Without the Registrar-General’s Department?

Yes, certain public institutions and special entities can register directly through GRA Taxpayer Service Centres using an introductory letter and approved supporting documents.

Why Is TIN or Ghana Card PIN Verification Important?

Verification helps institutions confirm the authenticity of a taxpayer’s identity, reducing fraud and ensuring compliance before financial or legal transactions are completed.

Can Banks or Institutions Apply for a TIN on Behalf of Clients?

Yes, selected mandated institutions can submit TIN applications for clients through special arrangements with the GRA to make compliance easier and faster.