A bill of exchange is a financial instrument that has been used for centuries to support trade, especially when buyers and sellers are separated by distance, borders, or legal systems. At its core, it is a written instruction that requires one party to pay a specific amount of money to another party, either immediately or on a future date. Although it may resemble an invoice or a simple request for payment, a bill of exchange carries formal legal weight once it is accepted by the party responsible for paying.

In modern commerce, bills of exchange are most commonly associated with international trade. They help bridge trust gaps between exporters and importers who may never meet in person. By clearly stating who must pay, who will receive payment, how much is owed, and when payment is due, the instrument brings structure and predictability to complex transactions.

How a Bill of Exchange Works in Practice

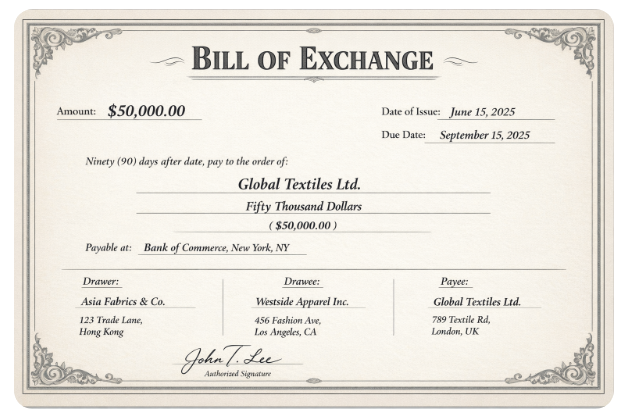

A bill of exchange begins its life when one party creates it and presents it to another. The party who writes the bill is known as the drawer. This drawer instructs another party, called the drawee, to make payment. The person or entity that ultimately receives the money is the payee. In many cases, the drawer and the payee are the same, but this is not always true.

Once the drawee formally accepts the bill, usually by signing it, the document becomes enforceable. From that point on, the drawee has acknowledged the obligation to pay the stated amount according to the terms written on the bill. Payment may be required immediately or after a defined period, depending on what the parties have agreed. This acceptance step is crucial. Without it, the bill of exchange is merely a request. With acceptance, it becomes a recognized promise to pay.

The Role of Timing and Payment Terms

One of the defining features of a bill of exchange is flexibility around timing. Some bills require payment as soon as they are presented, while others allow payment at a later date. The time between the issuance of the bill and the payment deadline is commonly referred to as the usance period.

In international trade, this delayed payment structure can be very useful. An importer may need time to receive goods, sell them, or process them before generating enough cash to pay the exporter. A bill of exchange can accommodate this need by allowing 30, 60, or 90 days before payment is due.

Unlike many loans, bills of exchange do not usually earn interest during this period. They function more like postdated payment commitments. However, if the parties agree that interest should apply in the event of late payment, this must be clearly stated on the document itself.

Why Bills of Exchange Matter in Global Trade

Cross-border trade involves unique risks. Buyers and sellers operate under different legal systems, currencies, and business norms. A bill of exchange helps reduce uncertainty by creating a clear, standardized payment obligation that is widely recognized across jurisdictions.

For exporters, the bill provides reassurance that payment has been formally acknowledged by the buyer. For importers, it offers time to manage cash flow without needing to pay immediately upon shipment. This balance makes the bill of exchange a practical compromise between trust and flexibility.

Additionally, because bills of exchange can be transferred to third parties, exporters may use them as financing tools. For example, an exporter might sell an accepted bill to a bank at a discount to obtain immediate cash, rather than waiting until the payment date.

The Parties Involved and Their Responsibilities

Every bill of exchange involves at least two parties and sometimes three. The drawer initiates the bill and defines its terms. The drawee is the party expected to make payment. The payee receives the funds once payment is made.

When the drawer and payee are different, the bill becomes even more versatile. A drawer can transfer the right to receive payment to another party by endorsing the bill. This transferability allows bills of exchange to circulate within financial systems, making them valuable instruments for credit and liquidity.

Each role comes with responsibilities. The drawee must honor the payment once acceptance has occurred. The drawer, depending on the structure, may remain liable if the drawee fails to pay, especially if the bill is transferred to a third party.

Common Types of Bills of Exchange

Bills of exchange come in several forms, each designed to serve a specific purpose within trade and finance. One common type is the trade draft, which is issued directly by a seller rather than a bank. These are widely used in commercial transactions between companies.

Another variation is the bank draft. In this case, a bank issues the bill and guarantees payment. Because the bank’s reputation and credit stand behind the instrument, bank drafts are often considered safer and more reliable than trade drafts.

Bills can also be classified by when payment is required. A sight draft demands payment as soon as it is presented to the drawee. This format is often used when the seller wants to retain control over goods until payment is made. A time draft, on the other hand, specifies a future payment date, allowing the buyer time before settling the obligation.

A Realistic Trade Scenario

Imagine a textile exporter shipping fabric to a clothing manufacturer in another country. The exporter draws up a bill of exchange stating that the manufacturer must pay a fixed amount within 60 days. The manufacturer reviews and accepts the bill, confirming the obligation.

Once the goods are shipped, the exporter holds the accepted bill as proof of the manufacturer’s debt. If the exporter needs immediate funds, they may take the bill to a financial institution and sell it at a discount. The bank then collects the full amount from the manufacturer at maturity.

This arrangement benefits all parties. The exporter gains either assurance of future payment or access to early financing. The importer receives goods without needing to pay upfront. The bank earns a return by assuming the short-term credit risk.

How Bills of Exchange Differ From Checks

Although bills of exchange and checks may seem similar, they serve different purposes. A check is typically used for immediate payment and is drawn against existing funds in a bank account. It does not usually include future payment terms.

A bill of exchange, by contrast, can be structured for payment at a later date. It also formally documents a debt relationship between parties. While a check is a payment instrument, a bill of exchange functions as both a payment mechanism and a credit tool.

Another distinction lies in acceptance. A check does not require acceptance by the bank before it is valid, whereas a bill of exchange must be accepted by the drawee to become enforceable.

Comparing Bills of Exchange and Promissory Notes

Bills of exchange are often compared with promissory notes, as both involve promises to pay. However, the direction of obligation is different. In a promissory note, the debtor promises directly to pay the creditor. The obligation originates from the party who owes the money.

With a bill of exchange, the creditor issues the instruction to pay. The debtor accepts this instruction and becomes bound by it. This structure allows bills of exchange to involve more parties and to be transferred more easily than promissory notes.

Because of this flexibility, bills of exchange are especially useful in trade finance, where obligations may need to move between sellers, buyers, and financial institutions.

Legal Standing and Enforceability

A bill of exchange is not the same as a contract, but it can support one. Contracts define the broader relationship between buyer and seller, including quality standards, delivery terms, and dispute resolution. The bill of exchange focuses narrowly on payment.

Once accepted, the bill becomes a legally enforceable obligation. If the drawee fails to pay, the holder of the bill may have the right to pursue legal remedies. This legal clarity is one reason why bills of exchange have remained relevant despite the rise of electronic payments.

That said, the bill must meet certain formal requirements, such as clarity of amount, identification of parties, and signature, to be valid under commercial law.

Advantages and Limitations

Bills of exchange offer several advantages. They improve trust between trading partners, support flexible payment arrangements, and can be used as financial assets. Their long history means they are widely understood in international commerce.

However, they are not without limitations. The process of acceptance, endorsement, and presentation can be slower than modern digital payments. There is also credit risk if the drawee becomes unable or unwilling to pay at maturity.

As a result, bills of exchange are often used alongside other risk management tools, such as letters of credit or trade insurance.

The Broader Role of Bills of Exchange Today

While electronic payments dominate domestic transactions, bills of exchange continue to play an important role in international trade and trade finance. They provide a structured way to manage deferred payments and allocate risk among parties.

Their continued use reflects a balance between tradition and practicality. Even in an age of instant transfers, the need for clear, transferable payment obligations remains.

Final Thoughts

A bill of exchange is more than a simple payment request. It is a formal financial instrument that creates clarity, trust, and flexibility in commercial transactions. By binding one party to pay another at a defined time, it supports the flow of goods and services across borders.

Although it is not a contract on its own, it complements contractual agreements and helps ensure that payment obligations are honored. For businesses engaged in trade, understanding how bills of exchange work remains a valuable skill in navigating global commerce.

Frequently Asked Questions about Bill of Exchange

Who are the main parties involved in a bill of exchange?

There are usually three parties: the drawer who creates the bill, the drawee who is asked to pay, and the payee who receives the money. Sometimes, the drawer and payee are the same person or business.

Why are bills of exchange commonly used in international trade?

They help exporters and importers manage risk, build trust, and allow flexible payment timing when businesses operate across different countries, currencies, and legal systems.

How is a bill of exchange different from a check?

A check is meant for immediate payment from existing funds, while a bill of exchange can require payment at a future date and formally records a debt obligation once accepted.

Can a bill of exchange be transferred to someone else?

Yes, bills of exchange are transferable. The payee can endorse the bill to a third party, such as a bank, which is why they are often used as short-term financing tools.

Is a bill of exchange the same as a contract?

No, it is not a contract on its own. However, it supports and enforces the payment terms of a broader commercial contract between trading parties.