In everyday accounting work, accuracy depends not only on recording transactions correctly but also on carefully summarizing them. One of the most practical techniques used to achieve this accuracy is known as footing. Although the term may sound technical at first, it simply refers to the process of adding up figures in an account to understand where the account stands at a particular point in time. Footing plays a quiet but essential role in ensuring that financial records are complete, reliable, and ready for reporting.

At its core, footing is about totals. Every account in a ledger records increases and decreases using two sides: debits on the left and credits on the right. Over time, as transactions accumulate, these columns can contain many entries. Footing brings order to this activity by summing each column separately. Once these totals are known, accountants can determine the balance of the account, which is the figure that eventually appears in financial statements.

What Footing Means in Practical Terms

Footing refers to the act of calculating the total of all amounts entered in the debit column and the total of all amounts entered in the credit column of an account. These totals are usually written at the bottom of each column, after drawing a line to indicate that a calculation has been performed. The resulting figures are called footings because they appear at the “foot” or bottom of the account.

This process does not, by itself, give the final balance. Instead, it provides the two totals that are compared to determine whether the account has a debit balance or a credit balance. In this way, footing is a stepping stone between raw transaction data and meaningful financial information.

Why Footing Is Necessary in Accounting

The primary purpose of footing is to support the calculation of account balances. Financial statements such as the income statement and balance sheet do not list every transaction that occurred during the period. Instead, they present summarized balances for each account. Without footing, there would be no systematic way to arrive at those balances.

Footing also serves as a basic control mechanism. By adding each column separately, accountants can quickly spot unusual totals or discrepancies that may suggest posting errors. If totals seem inconsistent with expectations, the account can be reviewed before it affects reports or decisions. In this sense, footing contributes to both accuracy and confidence in the accounting records.

The Structure of Debit and Credit Columns

To understand footing fully, it helps to revisit how accounts are structured. Each ledger account is divided into two sides. The left side records debits, while the right side records credits. Depending on the nature of the account—assets, liabilities, equity, income, or expenses—debits and credits have different effects.

As transactions occur, amounts are entered on the appropriate side. Over an accounting period, an account may accumulate many debit entries, many credit entries, or a mix of both. Footing does not judge whether those entries are correct; it simply adds them up so that the overall position of the account can be determined.

The Step-by-Step Footing Process

The footing process follows a clear and logical sequence. First, all transactions for the period must be recorded and posted to the appropriate accounts. Only once posting is complete does footing begin. At that stage, the accountant adds together all amounts in the debit column. This sum represents the total debits for the account during the period.

Next, the same addition is performed on the credit column. The total credits are calculated and written beneath the last credit entry. A single horizontal line is often drawn above these totals to show that a mathematical operation has taken place. These two figures—the debit footing and the credit footing—are the foundation for determining the account balance.

From Footings to Account Balance

Once both columns have been footed, the account balance is calculated by comparing the two totals. The smaller total is subtracted from the larger one. The difference represents the balance of the account. This difference is then placed on the side with the higher total, because that side determines whether the account has a debit balance or a credit balance.

For example, if total debits exceed total credits, the account has a debit balance equal to the difference. If total credits are higher, the account carries a credit balance. A second horizontal line is typically drawn to indicate that the balance has been calculated. This visual structure makes it easy to see both the totals and the final balance at a glance.

A Simple Illustration of Footing

Consider an account used to track service equipment. Over the accounting period, several transactions are recorded. Some increase the value of the equipment and are entered as debits, while others reduce it and are entered as credits. After all transactions have been posted, the debit column contains four entries and the credit column contains two.

When footing is performed, the debit amounts are added together to arrive at a total of 75,500. The credit amounts are also added, resulting in a total of 36,000. These figures are written at the bottom of their respective columns. To find the balance, the smaller total is subtracted from the larger one. The difference of 39,500 is placed in the debit column, showing that the account ends the period with a debit balance of that amount.

Footing as a Foundation for Financial Statements

The balances derived from footing are not an end in themselves. They are used to prepare financial statements that summarize a company’s financial performance and position. Each account balance feeds into a larger report, whether it is part of revenues, expenses, assets, or liabilities.

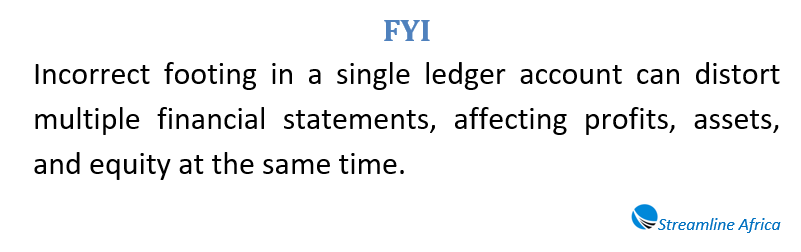

Because of this, errors in footing can have wide-reaching consequences. An incorrectly totaled account can distort profit figures, misstate asset values, or affect decision-making by management and stakeholders. For that reason, footing is treated as a routine but essential step in the accounting cycle.

Footing Versus Other Accounting Checks

Footing is often confused with other checking procedures, but it has a distinct role. Unlike a trial balance, which checks whether total debits equal total credits across all accounts, footing focuses on individual accounts. It does not test the overall equality of the ledger; instead, it ensures that each account has been summarized correctly.

Similarly, footing differs from cross-footing, which involves verifying totals across rows and columns in schedules or reports. While all these techniques support accuracy, footing is the most basic and frequently used method for ensuring that account-level data is reliable.

The Visual Importance of Lines and Totals

In manual accounting systems, visual cues play an important role. The lines drawn during footing are not decorative; they signal that calculations have been completed. A single line indicates that totals have been calculated, while a double line often indicates a final figure, such as a balance.

These conventions help anyone reviewing the account—whether an accountant, auditor, or manager—understand what has been done. Even in computerized systems, similar visual distinctions are used in reports to separate raw data from totals and balances.

Footing in Modern Accounting Systems

While many accounting systems are now automated, the concept of footing remains relevant. Software performs the arithmetic instantly, but the logic behind the process is the same. Debit and credit entries are accumulated, totals are calculated, and balances are derived.

Understanding footing is especially important when reviewing system-generated reports. Accountants who grasp the underlying process can better interpret totals, identify anomalies, and explain results to non-accountants. In this way, footing remains a foundational concept, even in a digital environment.

Common Errors Related to Footing

Despite its simplicity, footing can still be a source of errors. These may include adding incorrect figures, skipping entries, or misplacing totals on the wrong side of the account. Such mistakes can lead to incorrect balances that carry forward into financial statements.

To reduce these risks, accountants often recheck footings or use independent verification. In manual systems, this might involve recalculating totals. In automated systems, it may involve reviewing transaction listings to ensure that all entries have been captured correctly.

Educational Value of Footing

For students and new practitioners, footing is often one of the first accounting techniques learned. It reinforces the structure of accounts, the meaning of debits and credits, and the idea of balances. By practicing footing, learners develop a clearer understanding of how individual transactions accumulate into meaningful totals.

This educational value extends beyond bookkeeping. Even professionals who no longer perform manual footing benefit from having internalized the process, as it supports analytical thinking and error detection.

Why Footing Still Matters

Although it may appear to be a small procedural step, footing underpins the reliability of accounting information. It transforms lists of transactions into usable totals and balances. Without it, financial statements would lack a solid numerical foundation.

Footing also represents a broader principle in accounting: careful attention to detail. By methodically adding and comparing figures, accountants ensure that every amount has been accounted for and that the final numbers tell an accurate story about the business.

Bringing It All Together

Footing is the process of adding the debit and credit columns of an account to determine their totals and, ultimately, the account balance. It supports accurate reporting, helps detect errors, and ensures that financial statements reflect the true results of business activity. Whether performed manually or by software, footing remains a vital link between daily transactions and high-level financial information.

By understanding footing, one gains insight into how accounting transforms individual entries into clear, summarized figures. This understanding not only improves technical accuracy but also builds confidence in the financial data that organizations rely on to plan, decide, and grow.