In the world of statistics and data modeling, ensuring the accuracy and clarity of your results is essential. When working with multiple predictors in a regression model, one common issue that can distort your outcomes is multicollinearity. To address this, analysts rely on a helpful tool called the Variance Inflation Factor, or VIF.

What Is Variance Inflation Factor?

VIF is a diagnostic statistic used to assess whether independent variables in a regression model are too closely related. In simple terms, it checks if some variables are stepping on each other’s toes by carrying similar information. When predictors are too tightly connected, the model’s ability to distinguish their unique contributions becomes muddy, potentially leading to unreliable interpretations.

VIF evaluates how much the variance of an estimated regression coefficient increases due to collinearity among the predictors. In essence, the higher the VIF, the greater the inflation in variance—and that’s usually a red flag.

Why VIF Matters

Imagine building a model to determine what influences someone’s income. You might include education level, years of experience, and age. But if age and experience move in tandem, your model could struggle to figure out whether it’s age or experience driving the outcome. VIF helps reveal when this overlap is too strong.

When VIF values are high, the estimated coefficients of your predictors may swing wildly with small changes in data. That makes your conclusions wobbly. A model with low VIF values, however, tends to be more stable and trustworthy.

How Multicollinearity Affects Models

Multicollinearity refers to a situation where two or more predictors in your model are significantly correlated with each other. Although this doesn’t necessarily reduce the model’s ability to predict the outcome variable, it hampers your ability to interpret the individual effect of each predictor.

This tangled relationship leads to misleading or statistically insignificant results. It’s like trying to pinpoint which ingredient in a recipe adds sweetness when several ingredients are sugary. The model can still produce a decent cake, but good luck explaining what each ingredient did.

Common Symptoms of Multicollinearity

Some of the telltale signs of multicollinearity include:

- Large standard errors for regression coefficients.

- Unstable coefficients that change dramatically with minor adjustments to the model.

- A predictor that should be significant (based on theory or previous research) shows up as statistically insignificant.

When these issues arise, it’s crucial to dig deeper, and VIF is one of the first tools analysts turn to.

How to Detect Multicollinearity Using VIF

To determine whether multicollinearity is a problem, analysts calculate the VIF for each predictor variable. The basic formula for VIF is:

VIF = 1 / (1 – R²)

In this formula, R² is the coefficient of determination obtained when the predictor in question is regressed against all the other predictors in the model. Essentially, the formula checks how much of the variation in one predictor can be explained by the others.

If R² is high, the VIF will be high, signaling a potential multicollinearity problem.

Interpreting VIF Scores

Here’s how to interpret the values:

- VIF = 1: No multicollinearity. The predictor is entirely independent of the others.

- VIF between 1 and 5: Some correlation exists, but it’s typically manageable.

- VIF above 5: Indicates high multicollinearity. You may want to take action.

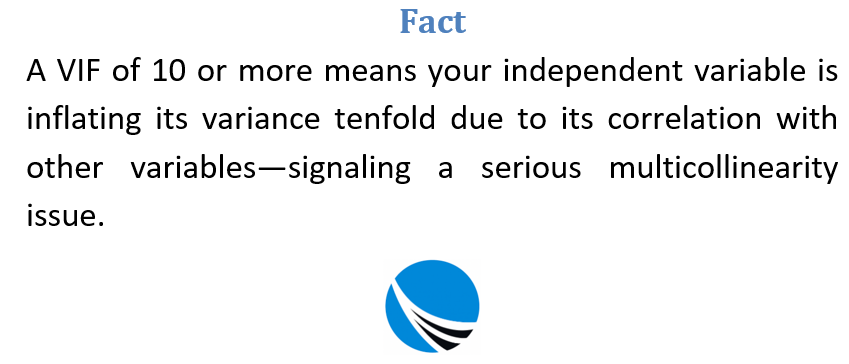

- VIF above 10: This level is generally considered severe and demands correction.

These thresholds are rules of thumb, and the appropriate cutoff may depend on the field or specific context of the analysis.

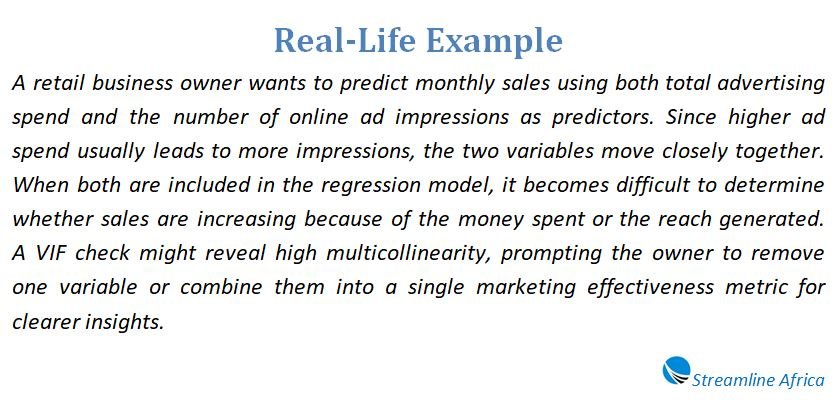

Example: Applying VIF in Practice

Suppose a researcher is analyzing how unemployment affects inflation. In the model, they include both the national unemployment rate and weekly jobless claims. These two indicators often move together, making them prime suspects for multicollinearity.

The model might still fit the data well overall, but VIF could reveal that one of the predictors adds little unique value. Removing one of the correlated variables could make the interpretation clearer without significantly hurting the model’s predictive power.

Strategies for Handling High VIF

When VIF reveals a high level of multicollinearity, several strategies can be used to address it:

- Remove one of the correlated variables: If two predictors are nearly identical in the story they tell, keeping both might not help.

- Combine the variables: Create a composite measure that captures the shared dimension.

- Apply dimensionality reduction techniques: Tools like Principal Component Analysis (PCA) or Partial Least Squares (PLS) can convert a set of correlated predictors into a smaller set of uncorrelated ones.

Each approach comes with trade-offs, but they can all help restore clarity to your model.

Limitations of VIF

While VIF is widely used and helpful, it’s not without its limitations. VIF only detects linear relationships among variables. It won’t catch nonlinear associations that could also cause issues. Also, decisions based solely on VIF might lead to oversimplification—removing variables that are actually important to your analysis.

Therefore, while VIF is an excellent first step, it should be used in combination with theoretical knowledge and other diagnostics.

When Low VIF Isn’t Enough

A low VIF doesn’t guarantee your model is flawless. It simply means multicollinearity isn’t a major concern. Other issues—like omitted variables, poor data quality, or irrelevant predictors—can still impair the performance or interpretation of your regression results.

A good analyst always balances statistical indicators like VIF with practical understanding and domain knowledge.

The Role of VIF in Predictive Modeling

In forecasting or predictive contexts, VIF is more about stability than interpretability. A model might still make accurate predictions even with high multicollinearity. However, if you’re building a model for decision-making or policy guidance, you’ll want to know what each variable is doing. That’s when keeping VIF low becomes a bigger priority.

Conclusion

Variance Inflation Factor is a powerful yet easy-to-use metric that reveals hidden issues in regression models caused by multicollinearity. By flagging variables that bring redundant information into the model, VIF helps analysts make informed decisions about which predictors to keep, merge, or drop altogether.

While some multicollinearity is expected and tolerable, high levels should prompt a reassessment of your model’s structure. With thoughtful adjustments—and possibly the aid of dimensionality-reducing techniques—you can ensure your regression model remains both predictive and interpretable.

In the end, understanding and applying VIF isn’t just a technical exercise; it’s about making your analysis sharper, your conclusions more reliable, and your decisions better informed.

FAQs about Variance Inflation Factor

Why does multicollinearity matter in a regression model?

Multicollinearity makes it hard to tell which variable is really influencing the outcome because the variables overlap in what they measure. This can lead to unstable and unreliable results.

What happens when VIF values are too high?

High VIF values indicate that a variable’s variance is being heavily influenced by other predictors. This usually means multicollinearity is present and needs to be addressed.

What’s considered a “bad” VIF score?

A VIF above 5 suggests a potential issue, and anything over 10 typically signals serious multicollinearity that should be corrected.

Can a model still work if multicollinearity exists?

Yes, the model might still predict well, but it’ll be harder to explain what each variable is actually doing. That’s a problem if you’re trying to make data-driven decisions.

How do you calculate VIF?

VIF is calculated using the formula: VIF = 1 / (1 – R²), where R² comes from regressing one predictor against all the others.

What should you do if VIF is high?

You can remove or combine the problematic variables, or use advanced techniques like Principal Component Analysis to reduce multicollinearity while keeping the model intact.

Does a low VIF mean my model is perfect?

Not necessarily. A low VIF only means multicollinearity isn’t a major issue. Other problems, like irrelevant variables or missing data, could still exist.

Can VIF detect nonlinear relationships?

No, VIF only checks for linear relationships between variables. It won’t catch nonlinear patterns that might also distort your model.

When should you care most about VIF?

VIF matters most when your goal is to interpret how each variable affects the outcome—not just when you want accurate predictions.