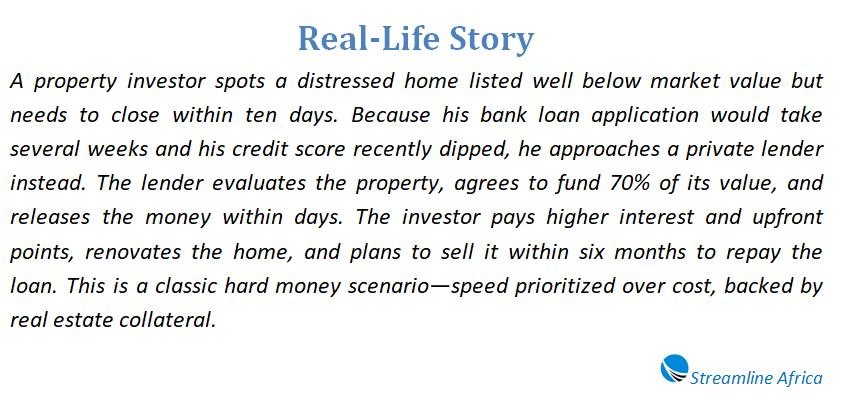

A hard money loan is a type of financing that relies primarily on physical assets, particularly real estate, as collateral. Unlike traditional bank loans that depend heavily on creditworthiness, these loans are issued by private lenders and focus on the value of the asset being offered. Because of this collateral-based nature, borrowers can access funds more quickly than with conventional loans.

This type of loan is often used when timing is critical or when traditional lending is out of reach due to credit issues. Businesses turn to hard money loans for real estate transactions, renovations, or other short-term capital needs that require speed and flexibility.

How Hard Money Lending Works

Hard money loans operate on a relatively simple principle: the value of the property or asset being pledged determines how much the lender is willing to offer. Typically, lenders assess what’s known as the loan-to-value (LTV) ratio—commonly 60% to 80% of the collateral’s current value. If the asset is valued at $200,000, for instance, the lender might offer a loan of $140,000 to $160,000.

What makes these loans attractive is how quickly they can be approved. Since lenders are not as concerned with the borrower’s financial history, approvals can sometimes happen in a matter of days.

However, this speed comes at a cost—literally. Borrowers usually pay higher interest rates (ranging from 8% to 15%) and upfront fees known as points (each point equals 1% of the loan amount).

Core Components of a Hard Money Loan

A hard money loan has three fundamental parts:

- Principal: The amount borrowed based on the asset’s value.

- Interest: The cost to borrow the money, which is usually much higher than what traditional lenders charge.

- Points: These are upfront fees paid to the lender. For example, a $100,000 loan with 5 points means a $5,000 fee paid at closing.

These terms vary by lender, and some may offer more flexible or lenient repayment options depending on the relationship with the borrower or the perceived risk.

Common Use Cases for Hard Money Loans

Hard money loans are ideal in situations where fast access to funding is more important than long-term cost. Common uses include:

- Acquiring time-sensitive real estate opportunities: Some business opportunities can’t wait for a bank’s lengthy approval process.

- Construction or renovation: Real estate investors often use these loans to rehab properties, especially when they plan to sell or refinance quickly.

- Working capital: When businesses need immediate cash flow to continue operations or pursue an opportunity.

- Bridge financing: Businesses waiting for long-term financing approval can use hard money loans as temporary stopgaps.

- Paying off existing obligations: Some use this method to consolidate or settle other high-interest loans temporarily.

Qualifying and Applying for a Hard Money Loan

Unlike traditional loans, hard money lenders don’t follow rigid lending criteria. Credit scores, income statements, and years in business are often secondary to the value and potential of the collateral.

To apply, businesses must:

- Identify a reputable private lender (either online or via local investor networks).

- Present a clear proposal including property details and the intended use of funds.

- Agree to an appraisal of the asset, which forms the basis of the loan offer.

- Review and sign a loan agreement, often within a few days of application.

Networking with real estate investors or joining local investment clubs can help connect you to trusted hard money lenders. Always research a lender’s reputation and licensing before proceeding.

Key Questions to Ask a Hard Money Lender

Before finalizing a loan, it’s essential to ask questions such as:

- What is the interest rate and how is it structured?

- How many points are charged at closing?

- Is there a prepayment penalty?

- What’s the loan term, and is it extendable?

- Does the loan cover renovation costs or just acquisition?

- Are repayments interest-only or include principal?

- How soon can funds be disbursed?

- What happens if you default on the loan?

The answers will help you assess the true cost and risks of the loan and ensure you’re entering the agreement with eyes wide open.

Pros of Hard Money Loans

There are several compelling reasons why businesses might opt for hard money lending:

- Speed: These loans can be secured quickly, sometimes within days—an advantage when time-sensitive deals are on the line.

- Flexibility: Fewer requirements related to credit history or income make hard money loans accessible to more businesses.

- Asset-focused: The loan approval depends primarily on the value of the property, not the borrower’s credit score.

- Less bureaucracy: Because they’re offered by private lenders, the process is generally simpler and faster.

These features make hard money loans particularly attractive for real estate investors or businesses needing short-term funds.

Cons and Risks of Hard Money Loans

Despite their convenience, hard money loans carry significant risks:

- High costs: Interest rates and points are often much higher than traditional loans, increasing the overall expense.

- Short-term nature: Loan terms typically range from 6 to 24 months, which can put pressure on businesses to repay quickly.

- Risk of foreclosure: If you default, the lender can seize and sell your property to recover their investment.

- Potential for predatory terms: Some lenders may include severe prepayment penalties or complicated terms, which could trap borrowers into extended high-cost debt.

Businesses should approach hard money lending with a well-structured repayment plan and a clear understanding of all terms.

When Hard Money Loans Make Sense

Hard money loans are not for every business, but they can be the right tool in specific scenarios:

- Credit issues: If a business owner has poor credit but valuable property, this type of loan offers access to financing.

- Multiple existing loans: Traditional lenders may limit the number of loans you can hold, but hard money lenders typically don’t.

- Urgent opportunities: When timing matters more than long-term cost, hard money loans shine.

- Short-term needs: If your financing need is temporary, and you can repay quickly, the higher costs may be acceptable.

In all cases, understanding your repayment strategy and sticking to it is vital.

Smarter Alternatives to Consider

While hard money loans serve a purpose, they’re not the only option. Depending on your situation, one of these might be more suitable:

- Equipment financing: Perfect for businesses purchasing machinery. The equipment itself serves as collateral.

- Invoice factoring: Offers fast cash by selling your outstanding invoices to a third-party for a fee.

- Short-term loans: Provide quick cash with less reliance on assets and often at better interest rates than hard money loans.

Each of these alternatives has its own set of pros and cons, and they often come with less severe repayment terms and lower risks.

Tips Before Accepting a Hard Money Loan

If you decide a hard money loan is right for you, keep these tips in mind:

- Avoid prepayment penalties: These are counterproductive in short-term lending situations.

- Know the details: Understand your interest rate, points, loan term, and whether payments are interest-only.

- Have a solid exit strategy: Whether you plan to refinance, sell a property, or repay using revenue, be clear about your plan.

- Prepare for the worst: Consider what you’ll do if the loan isn’t repaid on time—will you refinance, rent the asset, or sell another investment?

A disciplined repayment strategy is crucial to ensuring a hard money loan helps rather than harms your business.

Final Thoughts: Weighing the Benefits Against the Costs

Hard money loans offer speed, simplicity, and accessibility—especially for businesses in tight spots. But those benefits come at a price. High interest rates, aggressive repayment terms, and the risk of losing your collateral mean you must tread carefully.

Used wisely, these loans can bridge financial gaps, fund urgent projects, or help businesses that wouldn’t qualify for traditional loans. But misused or misunderstood, they can lead to serious financial strain.

Before signing any loan agreement, speak with legal or financial advisors. Make sure the terms align with your goals and capabilities. In the world of hard money lending, caution and planning are your greatest assets.

Commonly Asked Questions about Hard Money Loan

Who typically offers hard money loans?

Private individuals or non-bank institutions fund hard money loans. These lenders don’t operate like traditional banks and are often more flexible with their approval processes.

Why would a business use a hard money loan?

Businesses use hard money loans to access funds quickly—especially for real estate deals, renovations, or bridging a cash flow gap when conventional financing isn’t available.

How fast can you get approved?

Approval and funding can happen within days, much faster than the weeks or months it might take with a bank loan.

What’s the typical interest rate?

Interest rates usually range between 8% and 15%, which is significantly higher than most conventional business loans.

What are “points” in a hard money loan?

Points are upfront fees charged by the lender, typically 1% of the loan amount per point. For example, 3 points on a $100,000 loan means $3,000 due at closing.

How long do hard money loans last?

Most hard money loans have terms between 6 to 24 months. They’re designed for short-term use, not long-term financing.

Do I need good credit to qualify?

Not necessarily. These loans are asset-based, so lenders care more about the property’s value than your credit score.

What happens if I can’t repay on time?

The lender can seize the collateral—usually your property. That’s why it’s crucial to have a solid repayment plan in place before borrowing.

Are there alternatives to hard money loans?

Yes. Equipment financing, invoice factoring, and short-term business loans may offer more favorable terms depending on your needs and credit.

Is there a prepayment penalty?

Some lenders charge penalties for paying off the loan early. Always check the terms before signing to avoid surprise fees.

When does a hard money loan make the most sense?

It’s best when you need fast funding, have valuable collateral, and are confident in your ability to repay the loan within a short window.