What a Balance Sheet Represents

A balance sheet is one of the most important financial statements used in accounting. Often called a “statement of financial position,” it shows the resources a person, company, or organization owns and the obligations it owes at a single point in time. Unlike the income statement, which covers performance over a period, the balance sheet is a snapshot that captures financial health on a specific date—commonly at the end of a fiscal year or quarter.

For businesses, this document highlights three central categories: assets, liabilities, and equity. Assets represent what is owned, liabilities reflect obligations or debts, and equity shows the residual interest belonging to owners once debts are deducted. Together, these sections explain not only what an organization controls but also how those assets are financed—through borrowing or owner investment.

The Balance Sheet Equation

The foundation of every balance sheet rests on a simple yet powerful formula:

Assets = Liabilities + Equity

This equation must always remain in balance, which is where the name of the statement comes from. If a company buys equipment with borrowed money, both the asset side (equipment) and the liabilities side (loan) increase. If the company uses retained earnings to purchase assets, the equity side changes. This balancing mechanism ensures accuracy and accountability within financial reporting.

Understanding this equation helps stakeholders see where resources come from and how they are deployed. Investors may evaluate whether a company is too reliant on debt, while managers might assess how efficiently equity is being used to build long-term value.

Why the Balance Sheet Matters

The balance sheet plays a central role for a wide range of users. Investors examine it to judge whether a company is financially stable and capable of returning value. Creditors review liabilities and equity levels before extending loans. Regulators and tax authorities may require balance sheet data to ensure compliance.

For internal purposes, managers rely on it to make decisions about expansion, cost control, or debt repayment. Even individuals preparing a personal balance sheet can gain valuable insights into their financial standing, particularly when planning for major purchases or retirement.

By showing what is owned versus what is owed, the balance sheet also acts as an early warning system. Rising debt without matching asset growth, for instance, could signal potential liquidity problems.

Two Common Formats

Balance sheets are not always presented in the same way, but two primary formats dominate practice.

- Report form places assets at the top, followed by liabilities and equity below.

- Account form organizes assets on one side and liabilities with equity on the other, resembling a T-account in traditional bookkeeping.

While the layout differs, the information conveyed remains the same. Both formats must adhere to accounting principles and ensure that totals balance.

Personal Balance Sheets

Just as companies prepare balance sheets, individuals can also track their personal finances using the same approach. A personal balance sheet lists assets such as cash, investment accounts, and property. Liabilities may include credit card balances, student loans, or a mortgage.

By subtracting liabilities from assets, an individual determines their net worth. This calculation helps households understand whether they are building wealth or accumulating excessive debt. For instance, someone saving for a home can use their balance sheet to measure progress toward a down payment and assess whether liabilities are manageable.

Balance Sheets for Small Businesses

For small enterprises, a balance sheet serves as a crucial management tool. Typically, assets are grouped into categories like cash, receivables, inventory, equipment, and sometimes intangible assets such as patents. Liabilities include accounts payable, loans, and accrued expenses. The difference between these two sides shows the owner’s equity.

Small businesses often prepare balance sheets more simply than large corporations. Yet even a basic version can guide decisions, such as whether it is safe to take on additional debt, or if more equity funding is necessary. Footnotes may disclose contingent liabilities, like warranties, that don’t yet appear as current debts but could affect the future financial position.

Balance Sheets in Nonprofits and Charities

Not-for-profit organizations, particularly in certain jurisdictions like England and Wales, may submit a statement of assets and liabilities instead of a traditional balance sheet. This streamlined report lists significant holdings and obligations at the close of the year. Even though nonprofits don’t operate for profit, they still need to demonstrate stewardship of resources and accountability to donors, regulators, and beneficiaries.

Public Companies and Accounting Standards

For publicly traded companies, balance sheet presentation follows strict guidelines. In the United States, businesses must adhere to Generally Accepted Accounting Principles (GAAP), while international companies often follow International Financial Reporting Standards (IFRS).

Regulatory bodies such as the Financial Accounting Standards Board (FASB) in the U.S. or the International Accounting Standards Board (IASB) provide the framework. These rules ensure that balance sheets are comparable across industries and countries, giving investors a fair basis for analysis. Government agencies may use different rules altogether, focusing on accountability and transparency rather than profit.

Assets: What a Business Owns

Assets appear first on the balance sheet and are often divided into current and non-current categories.

- Current assets are expected to be converted into cash or used within a year. These include cash and cash equivalents, accounts receivable, inventory, and prepaid expenses.

- Non-current assets (or fixed assets) have longer lifespans. Examples include property, plant, and equipment, intangible assets such as patents or trademarks, long-term investments, and biological assets like orchards or livestock.

This distinction is crucial because current assets demonstrate short-term liquidity, while non-current assets reflect long-term investment in growth.

Liabilities: Obligations and Debt

Liabilities represent what a company owes to others. Similar to assets, they are classified as current or long-term.

- Current liabilities include obligations due within one year, such as accounts payable, wages, taxes, and short-term loans.

- Non-current liabilities extend beyond a year and may consist of bonds, leases, or pension obligations.

Some liabilities are contingent, meaning they depend on future events like lawsuits or warranty claims. These are usually disclosed in footnotes if they are probable and measurable.

Equity: The Residual Value

Equity, sometimes called net assets or shareholders’ equity, represents the owners’ claim after all liabilities are satisfied. In corporations, this includes common stock, additional paid-in capital, and retained earnings. In small businesses, it might simply be the owner’s capital account.

Equity is more than just an accounting entry—it reflects the cumulative value created by the business. Over time, reinvested profits grow equity, while losses or dividend distributions reduce it. Detailed disclosures within the equity section often include the number of shares authorized and outstanding, par values, treasury stock, and any restrictions on shares.

Net Current Assets and Working Capital

A key measure derived from the balance sheet is net current assets, also called working capital. This is calculated as current assets minus current liabilities. Positive working capital suggests a company can cover short-term obligations comfortably, while negative working capital may signal liquidity issues.

Investors and creditors pay close attention to this figure, as it often determines whether a company can sustain operations without additional borrowing.

Balance Sheet Substantiation

Behind every published balance sheet is a process known as substantiation. This involves reconciling the balances recorded in the general ledger with supporting documents, ensuring accuracy and compliance.

Substantiation is typically carried out monthly, quarterly, and annually. It includes reconciliations, review of documentation, and formal certification. Historically, this process relied heavily on manual spreadsheets, but automation tools are increasingly common, improving efficiency and reducing risk. Substantiation also plays a role in regulatory compliance, particularly under rules such as the Sarbanes-Oxley Act.

Technology and Modern Practices

In the past, preparing a balance sheet required painstaking manual calculations. Today, enterprise resource planning (ERP) systems like SAP or Oracle automate much of the process. Advanced software helps reconcile accounts, manage large volumes of data, and provide real-time insights.

These innovations reduce human error, speed up reporting cycles, and enhance transparency. For large corporations handling thousands of accounts, automation is no longer optional but essential.

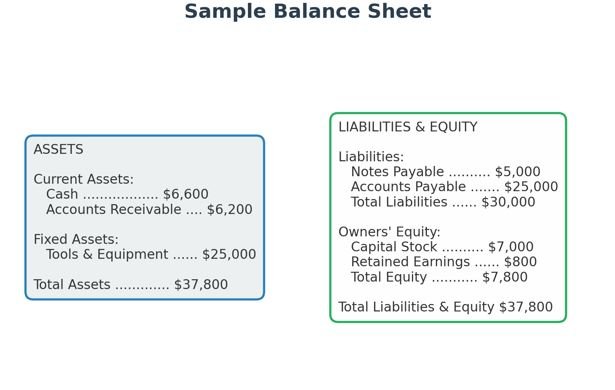

A Simplified Example

Consider a sample balance sheet prepared under IFRS. At the top, non-current assets such as land and buildings are listed, followed by more liquid items like cash. Liabilities start with accounts payable and progress to long-term debt. At the bottom sits equity, reflecting the owners’ residual claim.

Though simplified, this structure captures the essence of the balance sheet: showing where resources are tied up, how obligations are structured, and what remains for shareholders.

Interpreting Balance Sheets in Practice

While the document may look straightforward, interpretation requires nuance. A company with significant assets might still struggle if most are illiquid, such as specialized machinery. High equity might suggest financial strength, but it could also reflect a lack of dividend payouts. Similarly, large liabilities could be risky, yet in some cases, borrowing funds to expand operations is a strategic choice.

Analysts therefore look at balance sheets in context, comparing figures across multiple years and against industry benchmarks. Ratios such as the debt-to-equity ratio, current ratio, and return on equity provide deeper insights.

Conclusion

A balance sheet is far more than just numbers on a page. It tells the story of how resources are managed, how obligations are met, and how value is created for owners or stakeholders. Whether for a global corporation, a small family business, a nonprofit, or an individual household, the balance sheet remains an indispensable tool for understanding financial health.

By mastering this statement, anyone—from investors to everyday individuals—can make more informed decisions, spot warning signs early, and better plan for the future.

Balance Sheet – Frequently Asked Questions

Why is a balance sheet called a snapshot?

It’s called a snapshot because it reflects financial position at a single moment, unlike other statements that track performance over a period.

Read Also: Mastering Financial Statements: Guide for Investors, CEOs, and Analysts

How is a balance sheet structured?

Assets are listed on one side, while liabilities and equity appear on the other. The two sides must balance according to the accounting equation.

What is the accounting equation?

The equation is: Assets = Liabilities + Equity. It ensures that everything a business owns is financed either by debt or the owners’ money.

What are current assets?

Current assets include items like cash, receivables, and inventory that can be converted into cash within a year.

What are non-current assets?

These are long-term resources such as property, equipment, investments, and intangible assets like patents or goodwill.

What counts as liabilities?

Liabilities are obligations the business must pay, such as loans, accounts payable, taxes due, or bonds issued.

What does equity represent?

Equity is the residual value after liabilities are subtracted from assets. It reflects owners’ claims and retained profits.

Do individuals also use balance sheets?

Yes, personal balance sheets track assets like savings and real estate against debts like mortgages and loans to show net worth.

How do charities use balance sheets?

Some charities may file a simplified statement of assets and liabilities, which works like a balance sheet but with fewer details.

Why is balance sheet substantiation important?

It’s the process of verifying that balances are accurate and supported by records, helping maintain transparency and meet regulatory standards.

How are modern balance sheets changing?

Automation and accounting software have made balance sheet preparation and reconciliation more efficient, reducing errors and improving control.