For small and growing businesses, keeping cash flow steady and working capital healthy can be a constant challenge. A single late payment, seasonal slowdown, or surprise expense can throw everything off balance. To run smoothly and grow with confidence, businesses need flexible tools that safeguard liquidity without stalling operations. In this guide, we’ll explore practical financial solutions that help protect your working capital, unlock much-needed cash, and keep your business agile in the face of uncertainty.

The Common Struggles with Working Capital

Running a business means navigating the unexpected. Cash inflows rarely arrive in sync with your outflows—wages, rent, supplier payments, and utility bills don’t wait for customers to settle their invoices. The challenge becomes even tougher during seasonal dips or when pursuing growth opportunities that require upfront investment. That’s where working capital steps in. It cushions your operations and gives you room to cover essential operational expenses, buffer delays in receivables, purchase inventory in advance of sales, act on limited-time discounts or offers, manage debt repayments, expand without straining reserves, and handle unexpected repairs or equipment needs. Strong working capital allows your business to survive the lean months and thrive in busy ones.

Inventory Financing: Funding Before Sales

One of the trickiest cash flow hurdles is needing to pay for inventory long before earning from it. This is particularly relevant for retailers, manufacturers, or wholesalers.

Purchase Order Financing

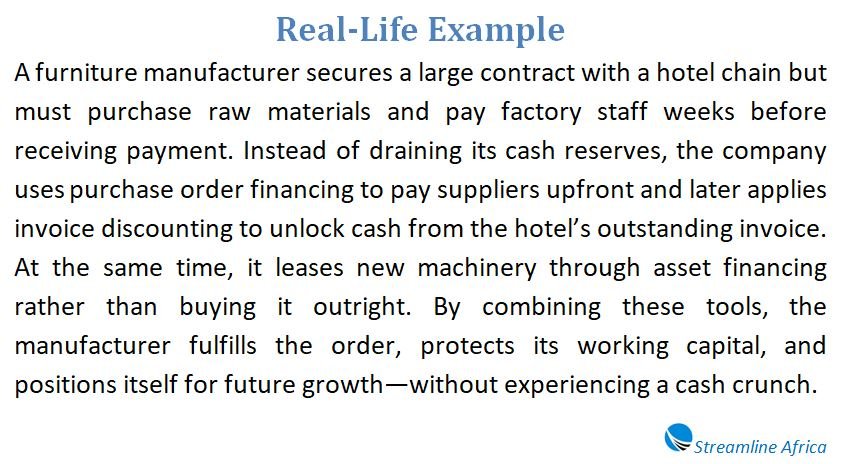

If you land a big customer order but don’t have the cash to pay your supplier upfront, purchase order financing (PO financing) could help. A finance provider pays your supplier directly. After the goods are delivered and you invoice your customer, the finance provider collects payment, deducts a fee, and sends you the balance. Approval is often based on your customer’s reliability—not yours—which is helpful for newer businesses. Just note that fees (1.8%–6% per month) can add up if your customer is slow to pay.

Overdrafts and Revolving Credit

Overdrafts allow you to draw beyond your bank balance when needed. You pay interest only on the overdrawn amount. Revolving credit offers similar flexibility but comes from external lenders rather than your bank account. Both are easy to access, but often carry higher interest rates and may require personal guarantees.

Improving Supplier Relationships with Supply Chain Finance

Supply chain finance lets suppliers get paid early by a third-party funder, while you repay the funder when the invoice matures. This benefits your supplier (who gains faster access to funds) and lets you hold onto your own cash longer. It strengthens relationships with key suppliers, enhances trust, and may even help you negotiate better pricing or delivery terms.

Asset Financing: Getting What You Need Without Draining Cash

Large purchases like vehicles, equipment, or software systems can eat into your working capital. Asset financing lets you access these essentials without needing all the money upfront.

Finance Lease

The finance provider buys the asset and leases it to you. You make monthly payments and handle upkeep. At the end, you may have the option to purchase it outright.

Operating Lease

Here, the provider maintains the asset, and you lease it for a defined period—often with the chance to upgrade before the lease ends.

Contract Hire

Common for fleet vehicles, this option includes maintenance. You simply pay a fixed monthly fee to use the vehicle.

Asset Refinancing

If you already own valuable assets, such as machines or trucks, you can release cash by refinancing them. The lender buys the asset and leases it back to you. You continue using it and regain ownership once repayments are complete. Asset-based financing is often easier to secure and doesn’t always require a strong credit score. However, you risk losing the asset if repayments aren’t met.

Late Payments: Unlocking Cash from Outstanding Invoices

Late customer payments remain one of the biggest threats to business cash flow. Fortunately, you can tap into the value of unpaid invoices to stay liquid.

Invoice Finance

Invoice factoring and discounting allow you to borrow against your receivables. With factoring, the financier collects from your customers. With discounting, you remain in charge of collections. This option is best for B2B companies with a consistent invoice flow. But if customers typically take more than 90 days to pay, lenders may hesitate to offer financing.

Working Capital Loans

These short-term loans provide a quick funding boost for daily operations. Secured loans are backed by assets and tend to offer better rates. Unsecured loans require a personal guarantee and a strong credit score, but they are faster to process. Both options can bridge gaps in cash flow or support rapid scaling when the timing is right.

Alternative Tools to Preserve Working Capital

Not every solution involves traditional lending. Some modern finance models help preserve your working capital while improving customer experience or expanding payment flexibility.

Buy Now, Pay Later (BNPL)

By offering deferred payment options to customers, you may increase conversions—especially for higher-cost items. While your business gets paid upfront (minus a transaction fee), the customer spreads their payments over time. It’s important to factor in the provider’s processing fees (2%–8%), which can add up depending on sales volume.

Merchant Cash Advances

For businesses with regular card transactions, a merchant cash advance (MCA) offers a lump sum that you repay as a percentage of future card sales. MCAs don’t require collateral, making them accessible to businesses with limited assets. However, they often come with steep fees, and fluctuating daily sales can make repayment unpredictable.

Grants

Grants are one of the few funding options that don’t need to be repaid. These are often awarded by governments, nonprofits, or corporate partners for specific industries, activities, or demographics. While competitive and time-consuming to apply for, grants can be a huge boost. Some offer full funding, while others require you to contribute matching funds. Always check the fine print before applying.

Crafting the Right Cash Flow Plan for Your Business

Choosing the right approach depends on your operations, customer behavior, and how quickly you need access to cash. For instance, a fashion retailer might benefit from inventory financing or BNPL, a logistics firm might need contract hire for vehicle fleets, and a manufacturing company could leverage asset refinancing or invoice discounting. Don’t wait until you’re under pressure to explore options. Build a plan with flexible tools already in place, so you’re ready when needs arise—whether it’s a surprise order or a cash crunch. A well-managed working capital strategy will help you pay staff and vendors on time, avoid debt penalties, capitalize on sales opportunities, maintain solid business relationships, and weather unexpected storms with less stress.

Final Take-home

Managing your business’s cash flow is not just about staying operational—it’s about staying empowered. With the right mix of financial tools, you can create room to innovate, grow, and adapt to changing conditions. Whether you’re just starting out or looking to expand, there’s a range of solutions—from asset refinancing to BNPL and invoice financing—that can provide liquidity without compromising your stability. Cash flow is the heartbeat of your business. Keep it healthy, and everything else becomes easier to manage. Start planning today, so you’re ready for whatever tomorrow brings.

Frequently Asked Questions

How Can Small Businesses Cope With Seasonal Dips in Revenue?

Seasonal slowdowns can drain your cash. Having flexible funding like overdrafts or working capital loans can help bridge the gap without halting operations.

What If I Land a Big Order but Can’t Afford to Fulfill It?

Purchase order financing helps you cover supplier costs upfront. The lender gets paid when your customer does, giving you the freedom to take on large orders.

How Do I Get Access to Equipment Without Paying Everything Upfront?

Asset financing lets you lease or refinance equipment and vehicles. You spread out payments while still using the assets to run your business.

What Can I Do About Clients Who Always Pay Late?

Invoice financing allows you to turn unpaid invoices into immediate cash. This keeps money flowing while you wait for customers to pay.

Are There Options That Don’t Involve Taking on Debt?

Yes. Grants are a great option if you qualify, and Buy Now, Pay Later can boost sales while keeping your cash intact. These don’t add liabilities to your books.

Is a Merchant Cash Advance Right for My Business?

If you get steady card payments, it might be. You repay as a percentage of sales, so it’s flexible. But the fees can be high, so weigh your options carefully.

How Do I Decide Which Cash Flow Tool to Use?

It depends on your needs, customers, and industry. If you need short-term breathing room, revolving credit helps. For growth or equipment, asset finance might be better. The right mix depends on your goals.