Introduction to VAT

Value-added tax, commonly referred to as VAT, is one of the most significant consumption-based tax systems in the world. Unlike income tax, which targets earnings, VAT focuses on spending. It is applied at different stages in the production and distribution process, whenever value is added to a product or service. By the time the consumer makes the final purchase, the tax has already been embedded into the price. This makes VAT a powerful tool for governments to collect revenue, but also a subject of much debate regarding fairness, efficiency, and its economic impact.

Globally, VAT is known by different names. In countries such as Canada, Australia, and New Zealand, it is typically referred to as the Goods and Services Tax (GST). While the terminology varies, the principle remains the same: every step in the supply chain, from manufacturer to wholesaler to retailer, remits a portion of the tax based on the value added at their stage. The consumer, however, ultimately bears the full cost.

The Origins of VAT

The concept of taxing value rather than turnover has roots in early 20th-century Europe. In 1918, German businessman Wilhelm von Siemens proposed an alternative to the turnover tax, which was heavily distortionary. Although Germany did not act on his suggestion immediately, it laid the groundwork for future developments. The first practical application came decades later in France, under the guidance of tax official Maurice Lauré. In 1954, Lauré introduced VAT in the Ivory Coast, then a French colony. After its success, France adopted VAT domestically in 1958.

The idea spread rapidly across Europe, particularly after the creation of the European Economic Community (EEC). In 1967, the EEC issued directives recommending VAT as the preferred indirect tax for member states. Over the following decades, virtually every European country adopted VAT, making it the backbone of public finances. Today, VAT is one of the world’s most widespread forms of taxation, implemented in more than 170 countries.

How VAT Functions

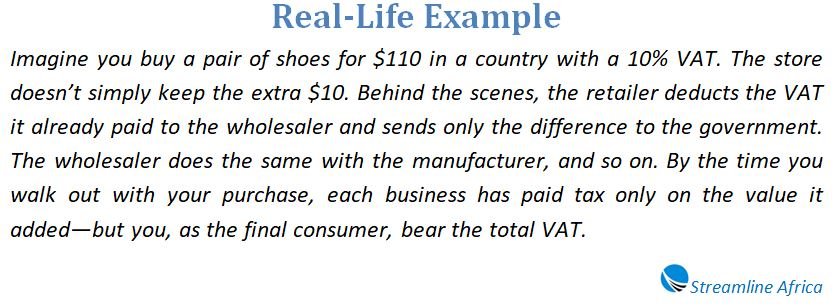

VAT operates on a simple principle: businesses collect tax on their sales (output tax) but can deduct the VAT they have already paid on their purchases (input tax). The difference is what they remit to the government. This system ensures that tax is collected in increments as products move through the supply chain.

For example, imagine a furniture manufacturer buying wood for $100 with a 10% VAT included. The manufacturer pays $110 to the supplier, of which $10 goes to the government. If the manufacturer then sells a chair to a retailer for $200 plus VAT ($220 total), the manufacturer keeps $200 but owes the government $20 in tax. However, they can deduct the $10 already paid on the wood, so they only remit $10. The process continues until the consumer pays the final price with VAT included.

This mechanism prevents double taxation, which can occur under simple sales taxes, and allows transparency in how much tax is collected at each stage.

VAT Compared to Sales Tax

The distinction between VAT and sales tax is crucial. Sales taxes are charged only once, at the final retail stage. VAT, in contrast, is collected throughout the chain of production and distribution. While the ultimate amount collected may be similar, VAT ensures more accurate reporting because businesses have an incentive to keep receipts to claim credits for taxes they have already paid.

Another difference lies in administration. Sales taxes are usually collected at local or regional levels, such as in the United States, where state governments levy them. VAT is more commonly a national tax, which allows for uniformity across a country. This centralization helps reduce distortions in trade between regions.

Advantages of VAT

VAT has several advantages that explain its global popularity. Firstly, it is efficient in revenue collection. Because the tax is built into each transaction, evasion is more difficult compared to other forms of taxation. Secondly, VAT is considered less distortive to business decisions than other taxes, such as corporate or payroll taxes. Companies continue to make production and distribution choices based on efficiency rather than tax avoidance.

Another strength of VAT is its resilience. Consumption remains relatively steady even during economic downturns, ensuring governments still have a stable revenue source. For many countries, VAT represents a substantial portion of total tax income, sometimes nearly half of all government revenue.

Disadvantages and Criticisms

Despite its strengths, VAT is not without flaws. A primary criticism is that VAT is regressive. Since everyone pays the same percentage regardless of income, low-income households spend a higher proportion of their earnings on VAT compared to wealthier individuals. This means the poor bear a heavier burden relative to their resources.

Another concern is administrative complexity. Businesses must keep detailed accounts of VAT paid and collected, increasing compliance costs, particularly for small firms. Refund delays can also strain business cash flow, especially for exporters who operate in zero-rated sectors. Fraud, including carousel fraud in Europe, remains another persistent problem, where dishonest traders exploit refund systems to claim VAT credits they are not entitled to.

VAT in Practice: A Simple Example

To illustrate the mechanics of VAT, let’s walk through a simplified scenario.

A farmer sells wheat to a miller for $1 plus 10 cents VAT. The miller processes the wheat into flour and sells it to a baker for $2 plus 20 cents VAT. The baker uses the flour to bake bread and sells it to a supermarket for $3 plus 30 cents VAT. Finally, the supermarket sells the bread to a consumer for $5 plus 50 cents VAT.

Each participant remits VAT based on the value they added. The farmer sends 10 cents to the government. The miller collected 20 cents but deducts 10 cents already paid, remitting 10 cents. The baker adds 30 cents but deducts 20 cents, leaving 10 cents. The supermarket collects 50 cents but deducts 30 cents, sending 20 cents. In the end, the government receives $0.50—the same as if a 10% sales tax had been applied at the final sale—but with less opportunity for evasion along the way.

The Debate Around Regressivity

Critics argue that VAT unfairly impacts the poor, who spend a greater share of their income on taxable goods like food and clothing. Proponents respond that essential items can be taxed at lower rates or even exempted to ease the burden. Many countries adopt multiple VAT rates, applying reduced or zero rates to necessities while taxing luxury goods at the full rate. Additionally, governments can use social welfare programs to redistribute revenue collected through VAT, offsetting its regressive nature.

Deadweight Loss and Economic Impact

Any tax influences behavior, and VAT is no exception. When the price of goods rises due to VAT, demand can decline. This creates what economists call deadweight loss—transactions that would have occurred in a tax-free environment but no longer happen because the tax increases costs. However, compared to other taxes, VAT is generally considered less distortionary, as it applies evenly across the economy rather than targeting specific sectors.

VAT and International Trade

One of VAT’s most notable features is its treatment of exports and imports. Exports are typically zero-rated, meaning they carry no VAT, ensuring goods remain competitive abroad. Imports, however, are taxed at the destination country’s VAT rate, ensuring domestic producers are not disadvantaged. While this system promotes fairness in trade, some critics argue that VAT functions as a hidden tariff on imports.

In the United States, for example, manufacturers have long complained that foreign VAT systems create an uneven playing field, as U.S. exports face VAT abroad but imports enter the U.S. free from a federal VAT. Proposals for “border-adjusted taxes” have surfaced periodically, but the idea remains politically contentious.

VAT Across the World

VAT is one of the most widely adopted tax systems globally, though its design differs from country to country.

- European Union: The EU requires member states to maintain a minimum standard VAT rate of 15%. Most members have higher rates, with Hungary’s 27% being the highest. Essential goods like food and medicine are often taxed at reduced rates.

- New Zealand: Known for its simplicity, New Zealand’s GST has very few exemptions, making it easier to administer. At 15%, it raises significant revenue with relatively low compliance costs.

- China: VAT accounts for the largest share of government revenue. Since 2016, China has applied VAT broadly, replacing earlier business taxes.

- India: Introduced VAT in 2005, later replaced by the Goods and Services Tax (GST) in 2017, a unified system intended to simplify the country’s fragmented tax structure.

- United States: The notable outlier. Instead of VAT, the U.S. relies on state and local sales taxes. Discussions about a federal VAT have emerged, but strong opposition has prevented adoption.

Case Study: Ghana’s VAT and Additional Levies

In Ghana, VAT operates at a standard rate of 15%. However, additional levies, such as the National Health Insurance Levy (2.5%), and the Ghana Education Trust Fund Levy (2.5%), apply alongside VAT. Together, these create an effective burden higher than the headline VAT rate. Businesses must account for these separately, and they cannot claim input credits for the levies, adding to compliance complexity. Despite these challenges, VAT remains one of Ghana’s primary revenue sources.

VAT Refunds for Tourists

One interesting aspect of VAT is that tourists often qualify for refunds on certain purchases. Many countries allow non-residents to reclaim VAT paid on items like clothing, jewelry, or electronics. To do so, travelers must keep receipts and file paperwork before departure, usually at the airport. While not all VAT can be recovered, this system promotes tourism spending by making goods more affordable for visitors.

VAT in the United States: A Persistent Debate

The absence of VAT in the United States makes it an outlier among developed economies. Advocates argue that adopting VAT could provide the federal government with a stable source of revenue while simplifying the tax code. Critics counter that it would disproportionately affect low-income households and complicate the existing system of state and local sales taxes. Studies by think tanks such as the Brookings Institution and the Congressional Budget Office have produced mixed results, suggesting both benefits and drawbacks. Despite occasional political discussions, VAT remains unlikely to be introduced at the federal level in the near future.

The Pros and Cons Summarized

Benefits of VAT include reliable revenue, reduced opportunities for tax avoidance, and efficiency in collection. It can encourage saving, as taxation is tied to consumption rather than income.

Drawbacks include its regressive impact, higher compliance costs for businesses, and potential inflationary effects as businesses pass the tax onto consumers. Fraud and refund abuses also continue to challenge tax authorities.

The Future of VAT

As economies globalize and e-commerce expands, VAT faces new challenges. Digital services, such as streaming platforms and online advertising, often cross borders without clear points of taxation. Many countries now require multinational digital companies to register and pay VAT, but enforcement remains complex. Another issue is harmonization. With varying rates and exemptions, multinational businesses face a patchwork of rules, leading to calls for greater international cooperation.

Climate change policies may also shape VAT’s future. Some experts suggest differentiated VAT rates to encourage sustainable consumption—for instance, lower rates on eco-friendly goods and higher rates on carbon-intensive products.

Conclusion

Value-added tax is one of the most important pillars of modern taxation. Its spread from postwar France to over 170 countries highlights its effectiveness as a tool for raising revenue. Yet, its universal nature also sparks debates about fairness, complexity, and economic impact. While VAT ensures governments have a steady income, it also requires careful design to balance efficiency with social equity.

In an era where global trade, digital economies, and social inequality dominate political agendas, VAT will remain central to fiscal policy discussions. Whether praised as a fair and efficient system or criticized as regressive and burdensome, VAT’s influence on how societies raise and spend public funds is undeniable.

Frequently Asked Questions about VAT

How does VAT differ from sales tax?

Sales tax is only applied at the final retail stage, while VAT is collected throughout the supply chain. VAT makes evasion harder and spreads the tax across each transaction.

Who first introduced VAT?

VAT was first introduced in 1954 by French tax official Maurice Lauré. It later spread across Europe and is now used in more than 170 countries worldwide.

Why do governments prefer VAT?

VAT provides stable revenue, is harder to avoid than many other taxes, and has less impact on how businesses organize their operations compared to sales tax.

Why is VAT criticized as unfair?

Critics argue VAT is regressive, meaning poorer households spend a greater share of their income on it compared to wealthier people who save more of their earnings.

Can VAT be made fairer for low-income households?

Yes. Many governments reduce or eliminate VAT on essentials like food and medicine, or provide rebates and welfare payments to offset the burden.

How does VAT affect international trade?

Exports are usually zero-rated, keeping them competitive abroad, while imports are taxed at the destination country’s rate, ensuring fairness to domestic producers.

How much revenue does VAT generate globally?

VAT contributes about one-fifth of total government tax revenues worldwide and is the single largest revenue source for many countries.

Why doesn’t the United States use VAT?

The U.S. relies on state and local sales taxes instead of a federal VAT. Political resistance and conflicts with existing tax systems have prevented its adoption.

What challenges do businesses face with VAT?

Businesses must keep detailed records, file frequent returns, and manage input-output credits. Delays in refunds and fraud schemes also create risks.

Can tourists get VAT refunds?

Yes, many countries let non-residents claim refunds on goods like clothes or electronics bought during their visit, encouraging tourist spending.

What is the future of VAT?

VAT is evolving to cover digital services and global trade more effectively. Some countries are also considering green VAT policies to promote sustainable consumption.