In most organizations, costs do not always rise smoothly as work increases. Instead, many expenses behave in a “jumping” pattern—remaining stable for a period and then suddenly rising when work expands beyond a certain limit. These unique expenses are known as step costs. They exist because companies often need to add new resources in chunks rather than in tiny increments. If operations grow or shrink enough to cross a threshold, the related costs rise or fall abruptly.

Step costs have a meaningful place in financial planning because they affect how businesses evaluate growth opportunities and manage resource capacity. When managers fail to anticipate these cost jumps, profitability can be affected in unexpected ways. Understanding how they work helps companies plan production levels, staffing requirements, and pricing decisions more accurately.

What Step Costs Represent

Step costs refer to expenses that stay unchanged as long as business activity falls within a certain range. Once demand, production volume, or workload increases beyond that range, those costs rise in a sudden leap rather than gradually. They do not behave like traditional variable costs, which move proportionally with activity. Instead, they remain fixed for a period and then increase in blocks.

This behavior often shows up visually as a staircase: a horizontal line representing costs at a stable level, followed by a sharp upward movement as soon as a threshold is crossed. The reverse can happen when output falls—costs drop suddenly when the business no longer needs a particular resource.

These cost movements happen because many business expenses cannot be adjusted in small amounts. Staff, machinery, workspace, and certain service contracts all require companies to commit to them in whole units. As a result, crossing a new level of activity forces the organization to take on an additional chunk of cost.

Why Step Costs Matter for Business Decisions

Step costs play a major role in operational and financial planning because they heavily influence profit margins. A company may be operating comfortably within a certain activity range, but slight growth could push it into a new level of cost. When that happens, the organization must cover additional expenses automatically, whether the increase in demand is small or significant.

In situations where revenue from the additional activity is not enough to absorb the new cost block, profits can shrink rather than grow. This is why managers sometimes hesitate to expand production or push for higher volumes—they may prefer to stay within the existing cost structure to avoid a sudden drop in earnings.

The same logic applies in reverse. When activity declines, reducing step costs can help protect the company from suffering unnecessary financial strain. Employers may downshift resources—such as cutting a shift or reducing space—to bring costs down to match lower demand.

Understanding when these jumps occur allows businesses to prepare for them, plan resource allocation wisely, and avoid financial surprises.

How Step Costs Influence Daily Operations

Step costs create a pattern of smooth operations followed by sudden shifts. For a certain level of activity, expenses hold steady. When the business crosses the threshold into a higher range, it must acquire additional resources to keep up with demand. These new resources might be in the form of labor, equipment, or production facilities.

During the period before a threshold is reached, the company benefits from operating efficiently without extra costs. Once activity pushes past the limit, the jump can be significant and immediate. This imbalance can alter projected profitability. Managers need to evaluate carefully whether the expected increase in output is strong enough to justify the extra cost.

Sometimes the reverse pattern occurs—when demand decreases enough for the company to scale down operations, allowing step costs to fall sharply. This reduction can help preserve profitability during slower periods.

Because of these dynamics, management must be aware of upcoming thresholds before deciding to take on additional work or encouraging an increase in production. A poorly timed expansion could cause the company to incur a full new block of cost for only a marginal gain in revenue.

Real-World Examples of Step Costs

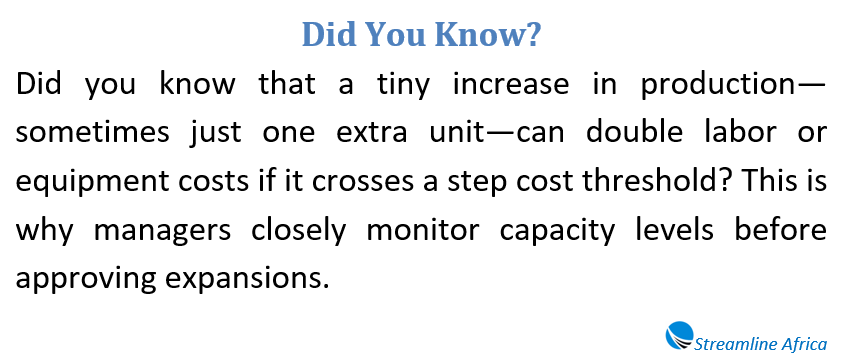

Step costs appear across industries and everyday business operations. Consider a technology company that produces advanced virtual reality headsets. The firm may be able to assemble 400 units within a single shift using a fixed number of employees and one supervisor. All costs associated with this shift remain the same whether the company produces 350 or 400 headsets.

However, if demand rises by even one more unit, the company cannot increase output without adding an entire second shift. This means hiring additional workers, bringing in another supervisor, and powering additional production hours. Suddenly, the cost to produce 401 units doubles from the cost required to produce 400. This dramatic leap reflects a classic step cost.

Another example occurs in a small coffee shop. With a single barista, the shop can comfortably serve a maximum of 30 customers an hour. As long as it stays within that range, labor costs remain unchanged. But once customer count reaches 31, the workload exceeds what one employee can handle. The shop must hire a second worker to maintain service quality. This new hire increases wage expenses and raises operating costs for the entire period when two employees are required.

In both scenarios, the cost increase is not triggered by a large change in demand—just a single unit or a few customers can push the business into the next cost level.

Managing Step Costs Strategically

Companies must take step costs into account when planning expansions, setting production levels, or introducing new services. If demand is rising but still relatively modest, it might not be wise to incur a large cost increase. Instead, businesses sometimes try to maximize efficiency within their current structure, finding creative ways to handle slightly higher workloads without committing to an entire new cost block.

However, if demand is strong and sustainable, taking on the higher step cost can be worthwhile. The additional revenue may not only cover the extra resources but also provide healthy profit margins over time. The key is evaluating whether the increased activity level genuinely justifies the cost jump.

On the other hand, when business activity slows down, managers may need to make difficult choices. They may scale back shifts, reduce staffing, or cut fixed commitments so that the business returns to a lower cost block. This flexibility helps companies stay financially stable during downturns.

Step costs therefore require careful monitoring and forecasting. Businesses need to determine the specific thresholds that affect their operations and plan accordingly.

Final Thoughts

Step costs represent expenses that do not move smoothly with operations but instead jump in response to changes in activity. Their staircase-like nature affects decisions about growth, scaling, staffing, and production. A company that understands these cost patterns can make smarter choices about when to expand and when to hold back. By analyzing the thresholds that trigger step costs, businesses can protect profitability and navigate operational changes more effectively.

Step Costs – Frequently Asked Questions

Why do businesses encounter step costs?

Many resources—such as staff, machinery, or workspace—cannot be added little by little. They must be added in whole units, which creates sudden cost jumps as activity increases.

How do step costs differ from variable costs?

Variable costs change proportionally with activity, while step costs stay fixed until a threshold is reached, then shift upward in a noticeable leap.

What happens if demand grows slightly but crosses a cost threshold?

Even a small increase can trigger a major cost jump. If the revenue from that increase is small, profits may shrink instead of grow.

Can step costs decrease as well?

Yes. If activity falls below a certain level, a business may cut shifts, reduce staffing, or scale back resources, causing step costs to drop suddenly.

Where do step costs most commonly appear?

You see them in manufacturing, service operations, retail staffing, facility usage, and any environment where resources are deployed in batches or units.

How can companies manage step costs wisely?

Businesses often monitor upcoming thresholds, improve efficiency to delay cost jumps, or make strategic expansions only when additional revenue clearly outweighs the new cost block.

Are step costs always bad for profitability?

Not necessarily. If demand is strong and sustainable, taking on a higher step cost can support growth and deliver higher long-term returns.

Why is understanding step costs important for planning?

Because ignoring step costs can lead to inaccurate budgets and unexpected profit swings, especially when activity levels hover near a threshold.

Can step costs influence pricing decisions?

Absolutely. If serving more customers requires a cost jump, companies may adjust pricing to ensure the new level of activity remains profitable.