An income statement, often referred to as a profit and loss statement or simply a P&L, is one of the cornerstone reports in financial accounting. It provides a clear view of how a business performs over a given period by showing the revenues earned, expenses incurred, and the resulting profit or loss. Unlike the balance sheet, which is a snapshot of financial health at a single point in time, the income statement tells a story of financial activity across weeks, months, or a fiscal year. This document is not just a regulatory requirement but a vital tool for managers, investors, creditors, and analysts who want to evaluate whether a business is thriving, struggling, or heading toward potential risks. By tracking the transformation of sales revenue—the so-called “top line”—into the “bottom line” net profit, an income statement makes it possible to assess efficiency, performance, and sustainability.

Why Businesses Use Income Statements

The primary function of an income statement is to demonstrate whether a business is making money. For entrepreneurs, this means understanding whether the company’s efforts translate into profits after subtracting costs. For investors, it signals whether a firm is worth supporting financially. Creditors also study it closely to judge whether a borrower is capable of repaying loans. Beyond these uses, income statements can highlight areas for improvement. For example, high operating expenses compared to revenue may suggest inefficiencies, while steady growth in profits could justify reinvestment or expansion. Essentially, the income statement helps stakeholders answer the critical question: Is this business financially healthy in terms of performance over time?

Differences from Other Financial Reports

The income statement is one of three major financial statements, alongside the balance sheet and the cash flow statement. While the balance sheet shows what a company owns and owes at a particular date, and the cash flow statement explains the movement of money in and out, the income statement concentrates on operations. For nonprofit organizations, a slightly different report is prepared, often called a statement of activities. Instead of focusing on profit, it outlines how funds from donors, grants, and other sources are allocated toward programs, administrative work, and other commitments.

Two Common Formats: Single-Step and Multi-Step

Companies can prepare income statements in more than one way. Single-Step Income Statement: This straightforward format adds up all revenues and subtracts all expenses to arrive directly at net income. While simple, it provides less detail about different stages of profitability. Multi-Step Income Statement: This version offers a layered breakdown. It begins with gross profit (revenues minus the cost of goods sold), subtracts operating expenses to find operating income, and then accounts for other revenues and expenses before deducting taxes to reach net income. This approach is more detailed and helps users understand exactly where profits are generated or lost.

Key Elements of an Income Statement

Though industries may vary, most income statements follow a common structure. Revenue refers to the money a company earns from its main operations—selling goods or providing services. Often labeled as “sales,” revenue is typically shown net of discounts, returns, and allowances. For most businesses, this is the first line on the statement, hence the term “top line.” Expenses reflect the costs associated with generating revenue. They may include wages, rent, utilities, marketing, and other outflows required to keep the business running. Cost of Goods Sold (COGS) for manufacturers and retailers measures the direct expenses tied to producing or purchasing inventory. It includes raw materials, labor, and production overheads. By subtracting COGS from revenue, a company determines its gross profit. Operating Expenses are the costs of running day-to-day operations outside of direct production. They can be divided into selling expenses (advertising, sales staff salaries, shipping) and general and administrative expenses (executive salaries, office rent, insurance, and utilities). Depreciation and Amortization spread the costs of long-term assets over time, reflecting wear and tear or the use of intangible assets like patents. Research and Development (R&D) captures spending on innovation. Non-Operating Items represent gains and losses not tied to core operations, such as currency fluctuations or interest expenses. Finally, Taxes are deducted before arriving at the net income.

Irregular and Special Items

Occasionally, companies must report unusual items that don’t reflect ongoing operations. These are separated out so users can evaluate performance without distortion. Examples include discontinued operations (selling or shutting down a segment), changes in accounting methods (switching from FIFO to LIFO), or rare events like natural disasters. These items help users distinguish between recurring performance and one-off shocks.

The Importance of Disclosures

Income statements rarely tell the full story on their own. Notes and supplementary disclosures provide context about unusual costs, asset write-downs, restructuring, or lawsuits. Without this information, the raw numbers might mislead stakeholders. Transparency through disclosure ensures comparability and reliability across companies.

Earnings Per Share (EPS)

One of the most critical figures that emerges from the income statement is earnings per share. It measures the portion of profit attributable to each share of common stock, giving investors a direct sense of value creation. EPS is calculated by dividing net income (after deducting preferred dividends) by the weighted average number of outstanding shares. Two types exist: basic EPS, which considers only existing shares, and diluted EPS, which assumes all convertible securities are exercised. Diluted EPS usually lowers per-share profit but is often seen as more conservative and realistic.

Sample Income Statement Structures

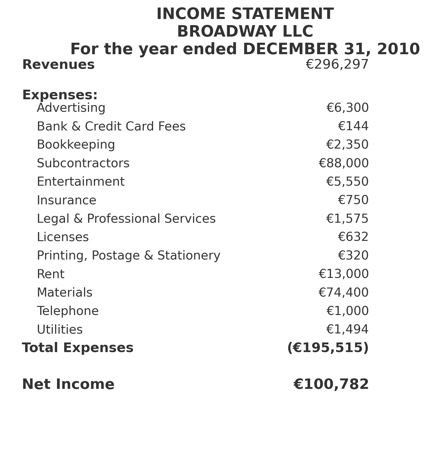

To better understand how numbers flow, consider two examples. A mid-sized manufacturing company might report revenue of £12 million, subtract COGS of £6 million, resulting in gross profit of £6 million. After deducting operating expenses of £3 million, interest costs of £200,000, and taxes of £1 million, the final net income could be £1.8 million. A global corporation may have revenues in the tens of billions, with detailed breakdowns for depreciation, impairment losses, discontinued operations, and results from affiliates. Though scale differs, the principle remains consistent: revenues flow downward, subtracting costs at each stage until arriving at the bottom line.

The Bottom Line Explained

The phrase “bottom line” refers to the net profit or loss recorded at the very end of the income statement. It is the ultimate indicator of whether the business added value during the reporting period. Investors and executives alike focus heavily on this number since it directly reflects shareholder returns and overall performance.

IFRS Requirements and Comprehensive Income

Under International Financial Reporting Standards (IFRS), companies must present not only an income statement but also comprehensive income. Comprehensive income combines net profit with “other comprehensive income,” which can include unrealized gains or losses on investments, currency translation adjustments, or revaluation of assets. Businesses may either prepare a single statement of comprehensive income or provide two separate statements: one income statement and one statement of comprehensive income. This ensures all non-owner changes in equity are captured, giving a more holistic picture of financial performance.

Limitations of the Income Statement

Despite its usefulness, the income statement is not flawless. Several limitations affect its accuracy and interpretation: it excludes factors that can’t be measured reliably, such as brand reputation or employee morale; results depend on accounting methods like FIFO versus LIFO; and many figures rely on estimates, such as depreciation schedules. Therefore, while the income statement is crucial, it must be analyzed alongside other reports and industry knowledge.

How Stakeholders Interpret It

Investors look at profitability trends and EPS to decide whether to buy, hold, or sell shares. Creditors assess whether a company generates enough profit to repay loans. Managers analyze margins and expenses to guide cost control and planning. Employees may see it as a reflection of company stability, influencing morale and job security. Each group extracts different insights, making the income statement a versatile but carefully interpreted document.

Practical Example: From Revenue to Net Income

Imagine a local restaurant with annual sales of €500,000. After subtracting food costs of €200,000, it has a gross profit of €300,000. From this, operating expenses such as wages, rent, and utilities total €220,000, leaving €80,000 in operating income. After accounting for €10,000 in interest and €15,000 in taxes, the restaurant’s net income stands at €55,000. This simplified flow mirrors how every business, from small enterprises to multinational corporations, uses the income statement to track performance.

The Income Statement as a Management Tool

For executives, the income statement is not just about compliance—it’s a compass for decision-making. By comparing current results with past performance, they can identify growth patterns or cost overruns. Budgeting and forecasting often rely on income statement trends to set realistic goals.

Looking Ahead: The Evolving Role of Income Statements

As business landscapes evolve, so too does financial reporting. Investors increasingly demand non-financial metrics, such as sustainability costs or social impact, alongside traditional income figures. While the income statement remains focused on profits, future adaptations may integrate broader indicators of corporate responsibility and long-term value creation.

Conclusion

The income statement remains one of the most powerful tools for understanding a company’s financial performance. From detailing revenues and expenses to highlighting the ultimate net income, it transforms raw financial activity into a story of progress, challenges, and outcomes. Though it has limitations and requires context from other reports, its ability to reveal profitability makes it indispensable for businesses, investors, and regulators alike. Whether for a small café owner tracking monthly performance or a multinational conglomerate preparing reports for global investors, the income statement continues to serve as a universal language of financial health and accountability.

Frequently Asked Questions about the Income Statement

Why is an income statement important?

It helps business owners, investors, and creditors understand if a company is profitable and where money is being earned or lost.

How is it different from a balance sheet?

The income statement tracks performance over time, while the balance sheet gives a snapshot of what a company owns and owes at a single point.

What does “top line” mean?

The top line refers to total revenue or sales before subtracting any costs or expenses.

What does “bottom line” mean?

The bottom line is the net income, showing the company’s profit after all expenses and taxes are deducted.

What are the two main formats of income statements?

The single-step format simply subtracts expenses from revenues, while the multi-step format breaks down gross profit, operating income, and net income.

What is gross profit?

Gross profit is revenue minus the cost of goods sold, showing how much a company makes from its core products or services before other expenses.

What are operating expenses?

These are day-to-day costs of running a business, such as salaries, rent, marketing, and utilities.

Why is depreciation included?

Depreciation spreads the cost of long-term assets like machinery or buildings over their useful life, making reporting more accurate.

What is earnings per share (EPS)?

EPS shows how much profit is allocated to each share of stock, helping investors judge a company’s value.

What are irregular or special items?

They are unusual events like selling part of the business, natural disasters, or changes in accounting rules, shown separately to avoid confusion.

How do disclosures add value?

Disclosures explain unusual numbers, lawsuits, or accounting changes, helping stakeholders understand the story behind the figures.

What are the limitations of income statements?

They rely on estimates, can be influenced by accounting methods, and don’t capture non-financial factors like brand strength.

How can businesses use income statements for decisions?

By comparing revenues and expenses over time, companies can control costs, plan growth, and forecast future performance.

Myths about the Income Statement

Income statements only matter for large corporations

Even small businesses and startups benefit from income statements because they reveal if the company is truly making money or overspending.

Profit on the income statement means plenty of cash

A company can show profit but still struggle with cash flow since the income statement doesn’t track when money actually comes in or goes out.

All expenses are easy to measure

Some costs, like depreciation or estimates for bad debts, involve judgment calls and aren’t always straightforward numbers.

The income statement tells the whole story

On its own, it can be misleading—real insights come when it’s combined with the balance sheet, cash flow statement, and disclosures.