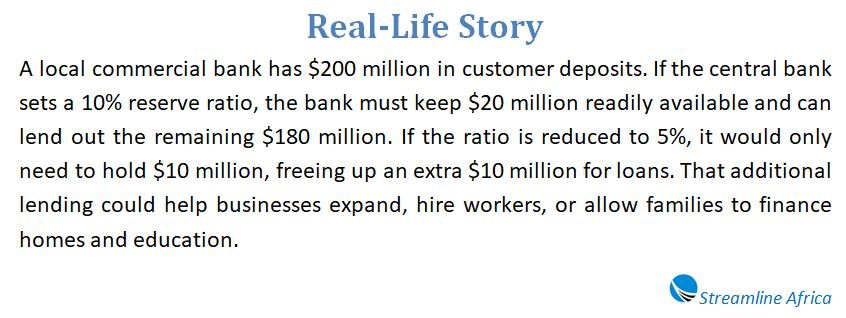

What the Reserve Ratio Means

The reserve ratio, sometimes called the cash reserve ratio, is a rule established by central banks that determines how much money commercial banks must keep on hand rather than lending out. In the United States, this is overseen by the Federal Reserve. The rule ensures that banks always have enough liquidity to handle customer withdrawals, while also serving as a lever for influencing the nation’s money supply. By adjusting this percentage, the Fed can encourage banks to lend more or restrict lending, thereby shaping interest rates, investment activity, and the overall pace of economic growth.

The reserve requirement—closely linked to the reserve ratio—is the actual dollar amount a bank must hold based on its customer deposits. Together, these measures play a vital role in balancing stability with growth in the financial system.

How the Reserve Ratio Is Calculated

The reserve ratio is relatively straightforward to calculate. A bank multiplies the amount of customer deposits it holds by the percentage set by the Federal Reserve. The result is the minimum cash it must keep in reserve.

For example, if the Fed required banks to hold 11% of deposits and a bank had $1 billion in deposits, it would need to keep $110 million in reserve. The remaining $890 million could then be lent to businesses and consumers, fueling economic activity.

This calculation highlights how a small change in the reserve ratio can significantly influence how much money flows into the economy.

Why the Reserve Ratio Matters for the Economy

The reserve ratio isn’t just a regulatory detail; it’s a powerful monetary policy tool. When the Fed lowers the ratio, banks are free to lend more of their deposits. This often leads to lower interest rates, easier access to credit, and stronger business and consumer spending. The economy tends to grow more quickly under these conditions.

On the other hand, raising the reserve ratio restricts lending. With fewer dollars available for loans, borrowing becomes more expensive, which slows down consumer purchases and business expansion. This tightening effect is useful when inflation is running too high, as it cools demand and helps stabilize prices.

The Reserve Ratio During Crisis

History shows that the Fed adapts reserve requirements to suit the needs of the economy. During the COVID-19 pandemic in March 2020, the reserve ratio was reduced to 0%. This unprecedented move was designed to make sure banks had no restrictions on lending, allowing money to circulate freely when businesses and households needed support most.

This decision demonstrated how central banks can use reserve requirements as a flexible tool to address urgent economic conditions, even if it means temporarily removing them.

The Link to Interest on Reserves

Since 2008, the Federal Reserve has paid banks interest on reserves they hold. Initially, there were two categories: interest on required reserves (IORR) and interest on excess reserves (IOER). These payments gave banks an incentive to maintain reserves while providing the Fed another way to influence monetary conditions.

In 2021, these categories were merged into a single measure called interest on reserve balances (IORB). As of mid-2023, the IORB rate stood at 5.4%. By paying interest, the Fed ensures that banks don’t see holding reserves as a disadvantage compared to lending, which strengthens stability in the financial system.

Current Regulations and Shifts Over Time

The Federal Reserve Board holds exclusive authority to change reserve requirements, but such changes must remain within limits established by law. Before the 2020 shift to 0%, banks faced different reserve levels based on deposit sizes. For instance, large institutions with more than $124.2 million in net transaction accounts once had to keep 10% of those funds in reserve. Mid-sized banks had lower percentages, while the smallest institutions had no requirement at all.

This tiered system acknowledged that smaller banks needed more flexibility, while larger banks had to contribute more toward overall system security. However, since 2020, reserve requirements for all categories have remained at 0%, allowing banks to fully use customer deposits for lending and investment.

Reserve Ratio and Fractional Reserve Banking

The reserve ratio is at the core of fractional reserve banking, the system under which modern banks operate. In this system, only a fraction of deposits are held in reserve, while the rest are loaned out. This process multiplies money in the economy.

Consider a scenario where a bank holds $500 million in deposits and faces a 10% reserve requirement. It would keep $50 million in reserve and lend $450 million. That $450 million would likely be deposited back into the system, allowing another bank to lend out 90% of it. The cycle repeats, creating multiple layers of new credit from the original deposit. This is known as the money multiplier effect, which shows how banking magnifies the supply of money available in the economy.

A Practical Example of Reserve Calculation

To calculate the reserve requirement, you simply convert the reserve ratio percentage into a decimal and multiply it by the deposit base. Suppose the ratio is 11% and deposits total $1 billion. Multiplying 0.11 by $1 billion yields $110 million, the required reserves. This straightforward math demonstrates how the central bank’s policy directly translates into operational requirements for financial institutions.

Why Central Banks Adjust the Reserve Ratio

Central banks adjust reserve ratios to manage risks and guide the economy. A lower ratio boosts lending, stimulates demand, and encourages growth. But if growth gets too fast and prices start rising uncontrollably, the Fed can raise the reserve requirement to rein in spending.

These adjustments also serve a protective purpose. By ensuring banks hold a certain percentage of deposits as cash, the system is better prepared for situations where many customers withdraw money at once. Without such safeguards, banks could face liquidity crises that might spill over into the wider economy.

Global Perspectives on Reserve Ratios

While this discussion focuses on the U.S., reserve ratios exist worldwide, though their levels and applications differ. Some countries maintain high ratios to protect against financial instability, while others set low or even zero ratios to encourage lending. The variation reflects each nation’s economic priorities, inflation risks, and financial system structures.

Criticisms and Limitations

Despite its importance, the reserve ratio isn’t a perfect tool. Critics argue that in today’s financial environment—where banks can borrow from central banks or access liquidity through other channels—the ratio plays a smaller role than in the past. Furthermore, setting it too high could unnecessarily restrict credit, while setting it too low might encourage excessive risk-taking.

Another limitation is timing. The reserve ratio affects banks gradually as lending and deposits adjust. For immediate influence, central banks often prefer interest rate policies, which can shift borrowing costs more quickly.

The Bigger Picture

Ultimately, the reserve ratio is one part of a broader toolkit used by central banks. While not always the most flexible instrument, it remains essential for maintaining balance in the banking system and preventing overextension of credit. By combining reserve policies with interest rate management and other monetary tools, the Federal Reserve and other central banks can guide economies toward both stability and sustainable growth.

Conclusion

The reserve ratio represents more than a technical banking rule—it is a cornerstone of monetary policy and financial security. By dictating how much of deposits banks must retain, central banks control the pace at which money enters circulation. When lowered, it stimulates lending and energizes growth. When raised, it slows activity to counter inflationary pressure. Even when set to zero, as seen during the pandemic, it highlights the adaptability of monetary policy to extraordinary circumstances. For banks, investors, and individuals alike, understanding the reserve ratio provides valuable insight into how the economy functions and how central banks work to balance stability with progress.

FAQs about Reserve Ratio

What is the reserve ratio?

The reserve ratio is the percentage of customer deposits that banks are required to hold in cash rather than lending out. It’s set by a country’s central bank to ensure stability and manage money supply.

Who sets the reserve ratio in the U.S.?

In the United States, the Federal Reserve determines the reserve ratio and adjusts it as part of its monetary policy tools.

How is the reserve ratio calculated?

You multiply the bank’s total deposits by the reserve ratio percentage. For example, if the ratio is 11% and deposits are $1 billion, the required reserve is $110 million.

Why does the reserve ratio matter?

It affects how much money banks can lend. A lower ratio means more lending and faster economic growth, while a higher ratio slows lending to control inflation.

What happened to the reserve ratio during the pandemic?

In March 2020, the Federal Reserve reduced the reserve requirement to 0% to ensure banks could lend freely and support the economy during the crisis.

What role does it play in fractional reserve banking?

The reserve ratio enables banks to lend out most of their deposits while holding only a fraction in reserve, creating a money multiplier effect that expands credit in the economy.

How does it influence inflation and growth?

When inflation is high, the Fed may raise the reserve ratio to reduce lending and cool the economy. When growth is sluggish, lowering the ratio encourages borrowing and spending.

Do banks earn interest on reserves?

Yes. Since 2008, the Federal Reserve has paid interest on reserves. In 2021, this was simplified into the Interest on Reserve Balances (IORB), which continues today.

What is the current reserve requirement in the U.S.?

As of 2024, the reserve requirement remains at 0%, meaning banks aren’t required to keep deposits at the Fed, giving them full flexibility to lend.

What are the criticisms of using the reserve ratio?

Some argue it’s less effective today because banks have other ways to access liquidity. Critics also note it can restrict credit too much if set too high or encourage risk-taking if too low.

Why should individuals care about the reserve ratio?

Because it indirectly affects interest rates, borrowing costs, and economic growth. Understanding it helps people anticipate changes in the financial system and their personal finances.