Introduction to the Cash Flow Statement

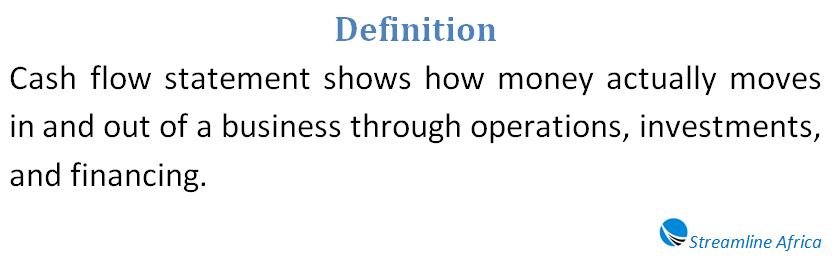

Among the most important tools for analyzing a business’s financial well-being is the cash flow statement. While the balance sheet and income statement are often given greater attention, the cash flow statement tells a story that those documents cannot fully capture: how money actually moves in and out of the company. It answers the critical question of whether a business generates enough cash to fund its day-to-day activities, meet obligations, and invest in growth.

Unlike profit figures, which can be influenced by accounting rules, the cash flow statement reveals a company’s liquidity in the purest sense. Investors, creditors, and managers all rely on it to evaluate financial health and sustainability.

What the Cash Flow Statement Shows

A cash flow statement summarizes the sources and uses of cash over a particular period, usually quarterly or annually. It separates these flows into three categories: operations, investing, and financing. By grouping transactions this way, stakeholders can see whether a business is primarily sustaining itself through its core activities, selling assets, or borrowing funds.

The overall result, called net cash flow, indicates whether cash increased or decreased during the reporting period. Even companies that report profits can experience serious challenges if they consistently have negative cash flows, which may threaten their ability to survive.

Why Cash Flow Matters More Than Profit

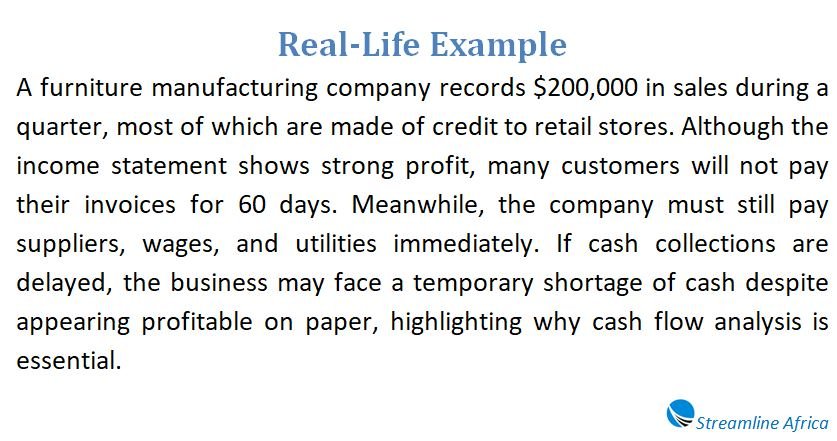

At first glance, profit and cash might seem like interchangeable terms, but in reality, they are different. Profit is based on accounting concepts such as accruals and deferrals. A company can record a sale today, recognize the revenue, and even pay taxes on it, but the actual cash may not arrive until months later.

Cash flow, on the other hand, reflects the immediate liquidity position. A company with strong profits but weak cash flow may struggle to pay salaries, purchase materials, or service debt. Conversely, a company might report modest profits yet enjoy strong cash inflows that allow it to expand. This is why analysts often look at the cash flow statement to validate whether earnings are backed by actual cash.

Historical Development of the Statement

The concept of tracking cash movement is not new. In the mid-19th century, the Dowlais Iron Company in Wales prepared what was effectively an early version of a cash flow report. Although profitable, the company lacked funds for a new furnace, and management created a statement to explain why cash was tight despite good results on paper.

Over time, regulators recognized the importance of standardized cash reporting. In the United States, the Financial Accounting Standards Board (FASB) introduced mandatory reporting rules in 1987 through Statement No. 95. Internationally, the International Accounting Standards Board (IASB) issued IAS 7, which became effective in 1994. These frameworks established the modern format still in use today.

Who Relies on Cash Flow Statements

Different groups depend on cash flow statements for varied reasons:

- Managers and accountants use them to ensure the business can cover payroll and operating expenses.

- Lenders and creditors assess repayment capacity.

- Investors evaluate whether earnings quality is high and whether dividends are sustainable.

- Employees and contractors gain confidence in the company’s ability to meet obligations.

- Directors and shareholders use the statement to monitor solvency and avoid trading while insolvent.

The versatility of this statement makes it one of the most valuable resources for both internal and external stakeholders.

Structure of the Cash Flow Statement

A standard cash flow statement is divided into three sections. Each highlights a different aspect of the company’s financial activity.

Operating Activities

The first section focuses on the company’s core business functions—producing goods, providing services, and managing day-to-day operations. It begins with net income and adjusts for noncash items such as depreciation, amortization, and changes in working capital.

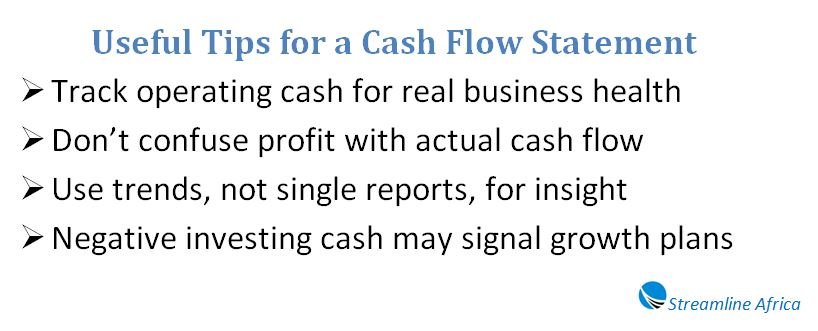

Operating cash flows include receipts from customers, payments to suppliers, wages, and taxes. They exclude investment or financing transactions. A consistently positive operating cash flow is generally a healthy sign, showing that the business model itself generates sufficient liquidity.

For example, if accounts receivable increase, it means more sales were made on credit, reducing actual cash inflows. Similarly, higher accounts payable may indicate that the company is delaying payments, temporarily boosting cash.

Investing Activities

The second section tracks how money is spent or received through investments. This includes purchases or sales of property, equipment, securities, and acquisitions. A negative figure in this section often suggests that a company is investing heavily in future growth, which may be viewed positively if aligned with strategy.

Conversely, positive investing cash flow may occur if a firm sells assets. While this boosts cash in the short term, relying too heavily on asset sales could signal difficulties in sustaining operations. Analysts therefore prefer to see modest, strategic use of cash in this area, balanced with strong operational inflows.

Financing Activities

The third section records how the company raises and repays capital. This includes issuing or repurchasing stock, borrowing funds, and paying dividends. A positive financing flow means the business is attracting external capital; a negative figure may mean debt repayments, dividend payouts, or share buybacks.

Neither positive nor negative is inherently good or bad. The context matters: raising funds might support expansion, while repaying debt strengthens the balance sheet. Investors closely watch this section to understand management’s financial strategy.

The Direct and Indirect Methods

Companies can prepare their operating cash flow section using two approaches.

- Direct method: Lists actual cash inflows and outflows such as receipts from customers and payments to suppliers. This method is straightforward and easier to understand but is less commonly used because it requires more detailed records.

- Indirect method: Starts with net income and adjusts for noncash items and working capital changes. Most companies use this approach because it ties easily to the income statement and balance sheet.

Regulatory bodies allow both methods, although under U.S. GAAP the indirect method is required as a supplement if the direct method is used.

Read Also: Top Strategies to Safeguard Cash Flow and Maximize Working Capital in Your Business

Indirect Method – Example

Cash Flow Statement (Indirect Method)

For the Year Ended December 31, 2024

Cash Flows from Operating Activities

Net Income: $120,000

Adjustments for Non-Cash Items:

- Add: Depreciation expense: $40,000

Changes in Working Capital:

- Increase in accounts receivable: ($50,000)

- Increase in inventory: ($30,000)

- Increase in accounts payable: 20,000

Net Cash Provided by Operating Activities: $100,000

Cash Flows from Investing Activities

- Cash paid to purchase property, plant, and equipment: ($150,000)

- Cash received from sale of property, plant, and equipment: 40,000

- Cash paid for investments: ($50,000)

- Cash received from sale of investments: 30,000

Net Cash Used in Investing Activities: ($130,000)

Cash Flows from Financing Activities

- Cash received from issuing shares: 200,000

- Cash received from borrowings: 100,000

- Cash paid for loan repayments: ($90,000)

- Cash paid for dividends: ($60,000)

Net Cash Provided by Financing Activities: $150,000

Net Increase (Decrease) in Cash and Cash Equivalents

$120,000

Cash and Cash Equivalents at Beginning of Period

$300,000

Cash and Cash Equivalents at End of Period

$420,000

Direct Method – Example

Cash Flow Statement (Direct Method)

For the Year Ended December 31, 2024

Cash Flows from Operating Activities

- Cash received from customers: $1,250,000

- Cash paid to suppliers: ($720,000)

- Cash paid to employees: ($280,000)

- Cash paid for operating expenses: ($90,000)

- Cash paid for income taxes: ($60,000)

Net Cash Provided by Operating Activities: $100,000

Cash Flows from Investing Activities

- Cash paid to purchase property, plant, and equipment: ($150,000)

- Cash received from sale of property, plant, and equipment: $40,000

- Cash paid for investments: ($50,000)

- Cash received from sale of investments: $30,000

Net Cash Used in Investing Activities: ($130,000)

Cash Flows from Financing Activities

- Cash received from issuing shares: $200,000

- Cash received from borrowings: $100,000

- Cash paid for loan repayments: ($90,000)

- Cash paid for dividends: ($60,000)

Net Cash Provided by Financing Activities: $150,000

Net Increase (Decrease) in Cash and Cash Equivalents

$120,000

Cash and Cash Equivalents at Beginning of Period

$300,000

Cash and Cash Equivalents at End of Period

$420,000

Indirect Method vs. Direct Method

| Section | Direct Method | Indirect Method |

|---|---|---|

| Operating Activities | Cash received from customers: $1,250,000 Cash paid to suppliers: ($720,000) Cash paid to employees: ($280,000) Cash paid for operating expenses: ($90,000) Cash paid for income taxes: ($60,000) Net Cash from Operations: $100,000 | Net Income: $120,000 Add: Depreciation: $40,000 Increase in accounts receivable: ($50,000) Increase in inventory: ($30,000) Increase in accounts payable: 20,000 Net Cash from Operations: $100,000 |

| Investing Activities | Net Cash Used: ($130,000) | Net Cash Used: ($130,000) |

| Financing Activities | Net Cash Provided: $150,000 | Net Cash Provided: $150,000 |

| Net Change in Cash | $120,000 | $120,000 |

| Ending Cash Balance | $420,000 | $420,000 |

Cash Flow Example in Practice

Consider a company that reports a net income of $120. If accounts receivable rise by $30, this amount must be deducted since it represents sales not yet collected in cash. If no other changes occur, operating cash flow would equal $90. This adjustment illustrates how accrual-based profit can differ significantly from cash reality.

Similarly, depreciation reduces profit but does not involve cash leaving the business. Therefore, it is added back to net income in the cash flow statement, ensuring the cash figure reflects actual liquidity.

Noncash Activities

Not all financing or investing actions involve cash. For example, converting debt into equity, acquiring assets through leases, or issuing shares in exchange for property are significant events but do not immediately affect cash balances. Standards require these transactions to be disclosed in the notes or within the statement itself, ensuring transparency.

International Differences

Although U.S. GAAP and International Financial Reporting Standards (IFRS) are broadly similar, some differences remain. Under IFRS, bank overdrafts may be included in cash equivalents, while under U.S. rules they are considered financing. IFRS also gives companies flexibility in reporting interest and dividends as either operating or financing activities, whereas U.S. GAAP generally classifies them as operating.

These differences underline the importance of understanding which accounting framework a company follows when analyzing cash flows.

How Investors Use Cash Flow Statements

For investors, the statement of cash flows provides insights that earnings reports cannot. A business consistently generating positive operating cash flow is generally more stable and less dependent on external financing. Conversely, if most cash comes from financing, it may signal overreliance on debt or equity issuance.

Investors also use the statement to assess dividend sustainability. A company paying out more than it generates in operational cash may eventually face liquidity issues, even if profits appear healthy.

Cash Flow and Company Strategy

Looking deeper, cash flow statements reveal management priorities. Heavy investment spending suggests a growth strategy, while significant debt repayments indicate a focus on financial stability. Similarly, large share buybacks may demonstrate confidence in the company’s valuation but also reduce available liquidity for expansion.

Understanding these movements helps stakeholders evaluate whether management’s actions align with long-term goals.

Common Misinterpretations

While valuable, the cash flow statement can be misunderstood. A negative cash flow from investing does not automatically indicate trouble—it may simply reflect expansion. Likewise, a positive financing cash flow might seem beneficial, but if it comes from repeated borrowing without operational improvement, it could signal risk.

Context and comparison over multiple periods are essential to draw accurate conclusions.

Limitations of the Cash Flow Statement

Despite its usefulness, the cash flow statement has limitations. It looks backward, summarizing what has already happened rather than predicting the future. It also does not capture non-financial factors such as market conditions, competitive dynamics, or management quality.

Therefore, analysts typically use it alongside the balance sheet, income statement, and broader industry information to gain a complete picture of financial performance.

The Bottom Line

The cash flow statement remains one of the most practical financial reports available. By categorizing cash movements into operations, investing, and financing, it highlights a company’s real financial strength beyond accounting profits.

For managers, it is a roadmap for ensuring liquidity and planning growth. For investors, it is a tool to judge whether earnings translate into tangible value. And for creditors, it reassures them of repayment capacity.

Ultimately, businesses that consistently generate healthy operating cash flows are better positioned to survive downturns, expand strategically, and reward their stakeholders. Understanding how to read and interpret this statement is therefore an essential skill for anyone engaged in business or finance.

FAQs about Cash Flow Statement

Why is cash flow more important than profit?

Profit can exist on paper, but without real cash coming in, a business can’t pay bills or grow.

Who uses a cash flow statement?

Managers, lenders, investors, employees, and shareholders all rely on it to judge financial health.

How is the statement structured?

It’s divided into operating, investing, and financing sections, each showing different cash movements.

What do operating activities include?

They cover everyday business tasks like customer payments, supplier costs, wages, and taxes.

Why might investing cash flow be negative?

Because the company is spending on future growth—like buying equipment or property—which can be a good sign.

What does financing cash flow reveal?

It shows how a business raises or repays money, like through loans, dividends, or issuing stock.

What’s the difference between the direct and indirect methods?

The direct method lists actual cash in and out, while the indirect method adjusts net income for noncash items and working capital changes.

Can noncash activities affect cash flow?

Yes—things like converting debt to equity or leasing assets matter, even if no money changes hands.

How do international rules differ?

U.S. GAAP and IFRS treat some items differently, such as overdrafts and how interest/dividends are classified.

How do investors use cash flow statements?

They check if profits are backed by real cash, if dividends are sustainable, and whether the company relies too much on borrowing.

What are the limits of a cash flow statement?

It looks backward, not forward, and can’t reveal market conditions, competition, or management quality.