When evaluating a company’s ability to meet its financial obligations, it is not enough to look at profits alone. Profit figures can be influenced by accounting adjustments, timing differences, and non-cash expenses. What truly matters when assessing whether a company can pay its debts is how much actual cash it generates. This is where the cash flow-to-debt ratio becomes particularly valuable. The ratio examines how well a business can use its operational cash inflows to manage and eventually repay the debt it owes, offering insight into financial stability and long-term solvency.

In essence, this ratio acts as a measure of debt repayment capacity. It shows how long it would take for a company to clear its debt if it dedicated all of its operating cash flow toward repayment. While companies rarely use all their cash flow for debt service, the ratio still provides a clear indicator of financial strength and risk exposure.

What the Cash Flow-to-Debt Ratio Represents

Every company needs to borrow at some point—whether to expand operations, buy equipment, or smooth out seasonal revenue fluctuations. Borrowing itself is not a problem; what matters is whether the business has the means to repay the debt without facing financial strain. The cash flow-to-debt ratio answers this question by comparing two critical numbers: the cash being generated by day-to-day operations and the total amount of outstanding debt.

If the ratio is high, it suggests that the company’s operations produce enough cash to manage repayments comfortably. Such companies usually have more flexibility, can tolerate periods of slower revenue, and may even be able to take on new borrowing if attractive investment opportunities arise. If the ratio is low, however, the company may struggle to meet its obligations, leaving it vulnerable in the event of unexpected downturns, rising interest rates, or tighter credit conditions.

The ratio tells a story about liquidity, risk management, and strategic capability. A strong ratio means lenders, investors, suppliers, and employees can all have greater confidence in the business’s resilience.

Key Concepts to Note

• The ratio uses operational cash flow, not net income, making it grounded in real inflows.

• A higher ratio reflects stronger debt management capacity.

• It can be used to estimate how long full repayment would take if operating cash were used exclusively.

• Comparisons across different industries require caution, because average debt and cash flow patterns vary widely.

• Analysts may also use free cash flow or EBITDA in place of operating cash flow, though each approach has different implications.

The Formula for Calculating the Ratio

The basic formula is straightforward:

Cash Flow-to-Debt Ratio = Cash Flow from Operations ÷ Total Debt

Here’s what each part means:

• Cash Flow from Operations refers to the cash generated directly from core business activities—primarily sales of goods and services, minus cash operating costs. It excludes investing or financing activities, ensuring the figure reflects only ongoing business performance.

• Total Debt refers to both short-term and long-term debt obligations. This includes bank loans, corporate bonds, credit facilities, and other forms of borrowing.

Total debt is used instead of only long-term debt because companies frequently use short-term financing to manage working capital or short-term projects. A ratio that accounts for all debt offers a more complete picture.

Why Cash Flow Offers Clearer Insight Than Net Income

It may seem intuitive to measure debt against profit, since profit indicates how much money a business makes. However, net income can be influenced by non-cash entries—such as depreciation, amortization, deferred revenue, or gains and losses from asset sales—that do not reflect actual cash movement.

For example, a company could show strong profits but still struggle to pay its debts if most of those profits remain tied up in inventory or unpaid invoices. Cash flow, on the other hand, tells us directly how much liquidity is available to actually make payments.

Using EBITDA or Free Cash Flow Instead

Some analysts use EBITDA (earnings before interest, taxes, depreciation, and amortization) in place of operational cash flow. Although EBITDA reflects performance before non-cash charges, it does not adjust for changes in working capital. If inventory rises faster than sales or receivables are slow to be collected, EBITDA may paint an overly optimistic picture.

Others prefer using free cash flow, which subtracts capital expenditures from operating cash flow. Free cash flow is more conservative because it accounts for reinvestments necessary to maintain or grow the business. Using free cash flow in the ratio may suggest that a company has less capacity for debt repayment, but it may give a more realistic long-term view.

Understanding What the Ratio Reveals

A ratio greater than 1.0 would indicate that a company generates more operational cash annually than the total amount of its debt—a sign of exceptional financial strength. However, this level is rare outside of industries with low leverage models.

More commonly, companies have ratios below 1.0. For instance, a ratio of 0.30 means the company generates operating cash equal to 30% of its total debt each year. If that level of cash flow remained consistent, it would theoretically take just over three years to pay down debt entirely.

However, the ratio should not be interpreted without considering industry standards. Utility providers or telecommunications firms, for instance, typically carry high levels of long-term debt but also generate steady, predictable cash flow. Meanwhile, industries such as technology or retail may have lower debt loads but greater variability in cash flow.

Thus, comparing a company only to others in the same sector leads to more meaningful conclusions.

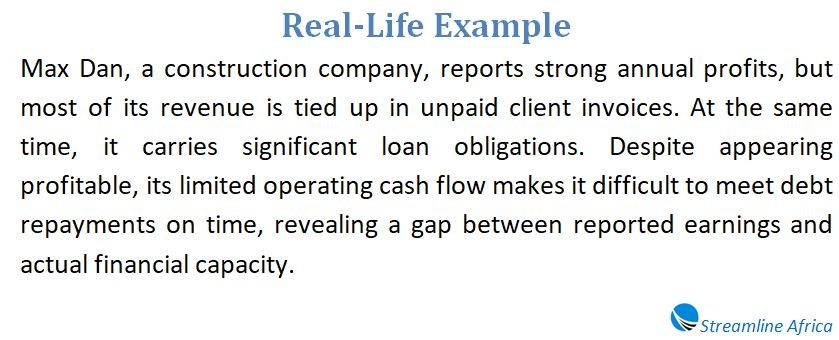

Practical Example

Consider a company named Horizon Manufacturing Ltd. Assume that during a given year, the company reports:

- Total debt: $2,000,000

- Operating cash flow: $500,000

Applying the formula:

Cash Flow-to-Debt Ratio = $500,000 ÷ $2,000,000 = 0.25 (or 25%)

This indicates that Horizon Manufacturing generates enough operating cash in a year to cover 25% of its total debt. If conditions remained stable, it would take about four years for the company to theoretically repay all of its debt. The calculation can be reversed to show this timeline:

1 ÷ 0.25 = 4 years

A ratio of 0.25 does not indicate distress. In fact, for many established companies, a ratio between 0.20 and 0.50 is common and acceptable. If Horizon’s ratio had been 0.50 or higher, it would suggest very strong liquidity and repayment capability. If the ratio were below 0.10, however, the company might face challenges if cash flows decline unexpectedly.

Why Trend Analysis Matters

A single ratio does not always provide the full picture. What matters just as much is how the ratio changes over time. A stable or improving ratio suggests the company is controlling costs, improving efficiency, or generating stronger revenue. A declining ratio may indicate rising borrowing costs, decreasing cash flow, or inefficient working capital management.

For lenders, investors, and management teams, a downward trend is a warning sign worth investigating.

Comparing Across Companies and Industries

Not all industries operate with the same financing structure. Capital-intensive sectors like transportation, manufacturing, and energy frequently rely on higher levels of debt to operate effectively. Meanwhile, service-based industries may carry much less debt and rely on fewer physical assets.

Thus, comparing the cash flow-to-debt ratio between companies in unrelated sectors can lead to misleading conclusions. A 0.30 ratio might be excellent in one industry and weak in another. This is why peer comparison is essential.

Final Thoughts

The cash flow-to-debt ratio plays an important role in evaluating a company’s financial strength. By comparing real operating cash flow to total debt, it gives a grounded view of whether a business can meet its obligations without relying on new financing or asset sales. A higher ratio generally indicates greater flexibility and lower financial risk, while a lower ratio signals the need to examine cash flow sources, debt structure, and operational efficiency.

However, no single ratio should be used in isolation. The cash flow-to-debt ratio becomes most meaningful when examined over time and compared with similar companies in the same industry. When interpreted thoughtfully, it serves as a valuable indicator of long-term financial stability and debt management effectiveness.