In everyday life, markets appear chaotic—prices rise and fall, shortages emerge, and surpluses pile up. Yet beneath this apparent disorder lies a powerful organizing principle: economic equilibrium. This concept explains how decentralized decisions by buyers and sellers can eventually align, creating a point where no participant has an immediate reason to change behavior. While the idea may seem abstract, it plays a critical role in understanding everything from food prices in Lagos to housing rents in Nairobi.

This reimagined exploration of economic equilibrium walks through its foundations, real-world applications, and limitations, using fresh examples and a narrative grounded in modern economic thinking.

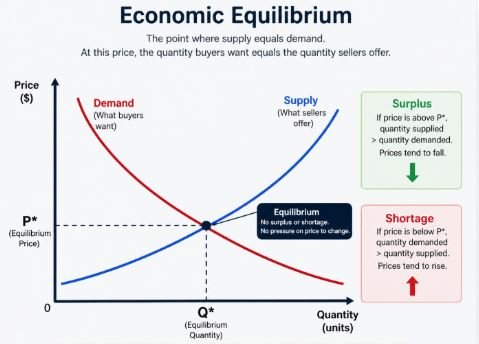

What Economic Equilibrium Really Means

At its core, economic equilibrium refers to a situation where opposing market forces—primarily supply and demand—are perfectly balanced. In such a state, the quantity of goods or services that producers are willing to supply matches exactly what consumers are willing to purchase at a given price.

Imagine a maize market in Kumasi. Farmers bring their harvest to sell, while traders and households arrive to buy. If the price is too high, maize remains unsold. If it’s too low, buyers compete aggressively, creating shortages. Over time, adjustments in price push the market toward a “clearing” point—where supply equals demand. That price becomes the equilibrium price, and the quantity traded becomes the equilibrium quantity.

At this point, there is no immediate pressure for change unless external conditions shift.

A Deeper Look: Stability and Behavior

Economists often evaluate equilibrium through three essential conditions. These principles help determine whether a market is not only balanced but also stable and sustainable.

First, participants must behave consistently. Buyers aim to maximize satisfaction (utility), while sellers aim to maximize profit. Second, no participant should have an incentive to change their decision at the prevailing price. If either buyers or sellers feel they could do better by acting differently, the system isn’t truly in equilibrium. Third, the equilibrium must be stable—it should naturally emerge through adjustments over time.

Consider a fish market in Dakar. If fish prices rise above the equilibrium level, fishermen bring in more supply than buyers want, creating excess stock. Prices then fall. Conversely, if prices drop too low, demand exceeds supply, pushing prices upward. This back-and-forth process gradually brings the market to a stable equilibrium—assuming no major disruptions.

Competitive Markets: Where Balance is Most Visible

In highly competitive markets, equilibrium is relatively straightforward. Prices adjust freely, and no single participant has the power to influence them significantly.

Take the example of a tomato market in Ibadan. Hundreds of farmers supply tomatoes, and thousands of consumers purchase them. Because no single farmer dominates the market, each accepts the prevailing price. At equilibrium, all tomatoes brought to market are sold, and all buyers willing to pay that price get their share.

This scenario satisfies the conditions of consistency and lack of incentive to deviate. Both buyers and sellers are optimizing given the price, and neither group has a reason to alter behavior. Moreover, the system tends to self-correct when disturbed, demonstrating stability. However, not all markets behave this neatly.

When One Player Dominates: Monopoly Equilibrium

Now consider a different scenario—a single electricity provider in a mid-sized city like Lusaka. Unlike competitive markets, this monopolist controls supply and can influence prices directly.

Instead of setting price where supply equals demand, the monopolist chooses output where profit is maximized. This occurs where marginal revenue equals marginal cost. The resulting price is typically higher, and the quantity lower, than what would occur in a competitive market.

In this case, equilibrium still exists, but it behaves differently. Consumers often wish to purchase more at the given price, meaning their incentives are not fully satisfied. The monopolist, however, has no reason to change strategy because profits are maximized.

This type of equilibrium highlights an important point: balance in economics does not necessarily mean fairness or efficiency.

Strategic Interaction: The Logic of Nash Equilibrium

Markets become even more complex when firms must anticipate each other’s actions. This is where the concept of Nash equilibrium becomes essential.

Imagine two competing cement manufacturers in Abidjan. Each must decide how much to produce, knowing that their decision will influence market prices and, in turn, the other firm’s profits. If one increases production, prices fall, affecting both firms.

A Nash equilibrium occurs when each firm chooses the best possible strategy given the other’s decision. Neither firm can improve its outcome by acting alone.

This concept is widely used in modern economics because many real-world markets involve strategic behavior rather than simple price-taking. However, the stability of such equilibria can be questionable, especially when firms continuously adjust strategies based on incomplete information.

The Mechanics of Market Clearing

To understand how equilibrium is determined mathematically, economists often use supply and demand equations. Suppose a local rice market in Tamale has the following relationships:

Qs=125+1.5PandQd=189−2.25P

Equilibrium occurs where quantity supplied equals quantity demanded. Solving this yields a price of approximately 17.07 (in local currency terms). At this price, the market clears—no surplus, no shortage.

If the price were higher, excess supply would emerge, forcing prices down. If lower, shortages would push prices up. This dynamic adjustment is central to how markets function.

Shifting Equilibrium: The Role of External Changes

Equilibrium is not permanent. It shifts when underlying conditions change.

For instance, imagine a sudden increase in household income in Accra due to a booming tech sector. Consumers now demand more goods at every price level. This shifts the demand curve to the right, leading to a higher equilibrium price and quantity.

Similarly, technological improvements—such as better irrigation systems in northern Ghana—can increase agricultural output. This shifts the supply curve outward, lowering prices and increasing the quantity traded.

These changes are analyzed using comparative statics, a method that compares one equilibrium state to another after a specific variable changes.

When Equilibrium Isn’t Ideal

A common misconception is that equilibrium always represents the best possible outcome. In reality, equilibrium can coexist with serious social issues.

Economist Paul Samuelson famously warned against assuming that equilibrium prices are inherently fair. For example, food markets can reach equilibrium even when some people cannot afford basic necessities.

A historical case is the Great Famine in Ireland, where food continued to be exported while locals suffered from starvation. Prices reflected global demand rather than local need, illustrating that equilibrium does not guarantee equitable outcomes.

Competing Views on Market Adjustment

Classical economists like Adam Smith believed markets naturally move toward equilibrium through price adjustments. Excess supply leads to falling prices, while shortages drive prices upward—eventually restoring balance.

However, modern economists have identified several exceptions. In labor markets, wages may remain above equilibrium due to policies or institutional factors, leading to persistent unemployment. In financial markets, banks may limit lending despite high demand, creating credit shortages.

These examples show that real-world frictions—contracts, regulations, and behavioral factors—can prevent markets from reaching equilibrium quickly, or at all.

Static vs Dynamic Equilibrium

Most introductory discussions focus on static equilibrium, where all variables remain constant over time. But economies are rarely static.

Dynamic equilibrium describes a situation where key variables—such as population, capital, and output—grow over time, but their relationships remain stable. For example, if both capital and labor grow at the same rate, output per worker may remain constant even as total production increases.

This concept is particularly relevant in growth economics, where long-term trends matter more than short-term fluctuations.

Disequilibrium: When Markets Are Out of Sync

Not all markets are in equilibrium at all times. Disequilibrium occurs when supply and demand are misaligned.

In fast-moving sectors like fuel markets, prices may lag behind global changes due to regulatory delays. In housing markets, long construction times can lead to prolonged shortages. Labor markets often experience persistent imbalances, with unemployment coexisting alongside unfilled vacancies.

These situations highlight that equilibrium is more of a tendency than a constant reality.

Final Thoughts: Equilibrium as a Framework, Not a Guarantee

Economic equilibrium provides a powerful lens for analyzing how markets operate. It explains how decentralized decisions can produce coordinated outcomes, even without central control. From local food markets to global industries, the concept helps economists predict how prices and quantities adjust over time.

However, equilibrium is not a promise of efficiency, fairness, or stability. It is simply a description of balance under specific conditions. Real-world complexities—monopoly power, strategic behavior, institutional constraints, and social inequalities—often distort or delay this balance.

Understanding equilibrium, therefore, is not about assuming markets always work perfectly. It’s about recognizing the forces at play, identifying when they fail, and designing better systems to address those failures.

Economic Equilibrium – Frequently Asked Questions

What does economic equilibrium actually mean in simple terms?

Economic equilibrium is the point where supply and demand meet perfectly. At this level, the quantity producers offer matches exactly what consumers want to buy, so prices tend to stabilize unless something changes.

Why do prices move toward equilibrium?

Prices adjust because of pressure from shortages and surpluses. If goods are scarce, prices rise; if there’s too much supply, prices fall. These movements naturally push markets toward balance.

Can a market be in equilibrium but still unfair?

Yes. Equilibrium only reflects balance, not fairness. As Paul Samuelson pointed out, markets can settle at prices that still leave some people unable to afford essential goods.

What makes a competitive market equilibrium stable?

A competitive equilibrium is stable when buyers and sellers have no incentive to change their decisions, and any disruption (like a price change) naturally corrects itself over time.

How is monopoly equilibrium different?

In a monopoly, one seller controls supply and sets prices to maximize profit. This often leads to higher prices and lower output compared to competitive markets, and consumers may feel underserved.

What is a Nash equilibrium and why does it matter?

It’s a situation where each participant makes the best decision based on others’ actions. It matters because many real-world markets involve strategic decisions, not just simple buying and selling.

What happens when equilibrium is disrupted?

When something changes—like income levels or production costs—the balance is disturbed. Prices and quantities then adjust until a new equilibrium is reached.

Is equilibrium always static?

No. In dynamic equilibrium, key variables like output and capital can grow over time, but their relationships remain stable. It’s common in long-term economic growth models.

What is disequilibrium and why is it important?

Disequilibrium happens when supply and demand don’t match. It’s important because it explains real-world issues like shortages, unemployment, and price volatility.