At the core of classical economic thinking lies a principle developed by Jean-Baptiste Say, a 19th-century economist who sought to explain how economies generate wealth. His idea, widely known as Say’s Law of Markets, proposes a straightforward but powerful relationship: the act of producing goods and services creates the income necessary to purchase other goods and services.

Rather than viewing money as the engine of economic activity, Say argued that real production is what drives demand. When individuals or firms create something of value and sell it, they earn income. That income then becomes purchasing power, enabling them to buy other products in the marketplace. In this way, economic activity becomes a continuous cycle of production and exchange.

This perspective challenges the notion that economies grow simply because people spend more money. Instead, it places productive capacity—what a society can create—at the center of long-term prosperity.

The Logic Behind Production Creating Demand

Say’s reasoning begins with a simple observation: people cannot consume unless they have first contributed something to the economy. A farmer sells crops, a manufacturer sells machinery, and a consultant sells expertise. Each transaction generates income, and that income becomes the basis for future spending.

In practical terms, this means that demand is not an independent force floating in the economy. It is directly tied to prior production. When businesses expand output, they pay wages, distribute profits, and purchase inputs. These payments flow through the economy, giving households and other firms the financial means to buy goods and services.

Money, in this framework, plays a supporting role. It acts as a medium of exchange, making transactions more efficient, but it does not create wealth by itself. Real wealth comes from goods and services produced, not from the accumulation of currency.

Say’s Law Versus Mercantilist Thinking

Say’s ideas emerged partly as a response to earlier economic doctrines that emphasized the accumulation of money and trade surpluses. Under mercantilist thinking, wealth was often equated with gold, silver, or positive trade balances.

Say rejected this view. He argued that focusing on money misses the bigger picture. An economy becomes richer not by hoarding currency but by increasing its productive capacity. Factories, farms, technology, and skilled labor are what truly expand wealth.

This shift in perspective has important implications. If production is the source of prosperity, then policies should encourage entrepreneurship, investment, and innovation rather than simply boosting consumption or restricting imports.

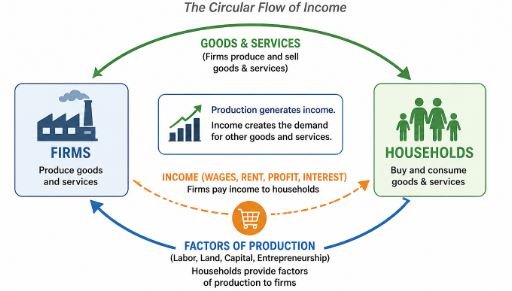

The Circular Flow of Income Explained

Say’s Law can be better understood through the concept of the circular flow of income. Imagine a simplified economy with two main participants: firms and households.

Firms produce goods and services and pay wages to workers. Those workers, in turn, use their income to purchase the goods produced by firms. The money spent by households becomes revenue for businesses, allowing them to continue production and pay wages again.

If production increases, wages and incomes also rise, enabling greater consumption. This creates a self-reinforcing loop where output and demand grow together. Although real-world economies are more complex—with savings, taxes, and international trade—this basic model illustrates the core intuition behind Say’s Law.

Key Implications for Economic Growth

Say’s framework leads to several important conclusions about how economies expand over time. First, growth is fundamentally driven by increases in production rather than increases in spending alone. A society that produces more goods and services naturally generates more income, which translates into higher demand.

Second, industries are interconnected. When one sector grows, it creates opportunities for others. For example, a thriving manufacturing industry increases demand for raw materials, transportation, and financial services. Economic success tends to cluster, with productive regions reinforcing each other’s growth.

Third, international trade can be beneficial even when a country imports more than it exports. Imports provide access to goods that might be costly or inefficient to produce domestically, allowing resources to be allocated more productively elsewhere.

Finally, policies that prioritize production—such as reducing barriers to business activity—are seen as more effective than those focused solely on stimulating consumption.

Modern Interpretations and Influence

Although developed in the early 1800s, Say’s Law continues to shape economic thought today. It is particularly influential among supply-side economists, who argue that economic policy should focus on improving the conditions for production.

Supply-side approaches often emphasize tax reductions, regulatory reform, and incentives for investment. The idea is that when businesses are encouraged to produce more, the resulting increase in income will naturally lead to higher demand and overall growth.

The principles of Say’s Law also align closely with the Austrian school of economics, which highlights the role of entrepreneurs in coordinating production and responding to market signals. From this perspective, economic imbalances are often traced back to distortions—such as artificial interest rates or excessive government intervention—that disrupt the natural flow of production and exchange.

Criticism from Keynesian Economics

Despite its influence, Say’s Law has faced significant criticism, particularly from John Maynard Keynes. In his seminal work, The General Theory of Employment, Interest and Money, Keynes challenged the assumption that supply automatically generates sufficient demand.

Keynes argued that economies can experience periods where total spending falls short of total production. During such times, businesses may be unable to sell all their goods, leading to layoffs, reduced income, and further declines in demand. This creates a negative feedback loop that can result in prolonged recessions.

One historical example often cited is the Great Depression, when high unemployment and weak demand persisted for years despite the economy’s productive capacity.

Keynes also pointed out that people do not always spend all their income. They may choose to save, especially during uncertain times. If those savings are not translated into investment, overall demand can fall short, contradicting the idea that production alone guarantees sufficient demand.

Situations Where Say’s Law May Break Down

In theory, Say’s Law assumes that markets adjust quickly to imbalances. If there is excess supply in one area, prices fall, encouraging consumption or redirecting resources to other sectors. However, in practice, several factors can disrupt this adjustment process.

One such factor is wage rigidity. Workers may resist wage cuts, preventing labor markets from clearing efficiently. Another is the tendency for individuals and businesses to hold onto cash during periods of uncertainty, reducing spending and slowing economic activity.

Financial crises can also amplify these effects. When banks and households focus on reducing debt rather than spending, the flow of income weakens. This dynamic was evident during the global financial downturn of 2008, when reduced lending and cautious consumer behavior contributed to a prolonged slowdown.

Additionally, situations like liquidity traps—where interest rates are very low but investment remains weak—challenge the assumption that savings will automatically be converted into productive activity.

The Role of Government Policy

The debate over Say’s Law often centers on the appropriate role of government in the economy. If one accepts Say’s argument, minimal intervention is preferred. Markets, left to their own devices, will coordinate production and demand efficiently over time.

However, Keynesian economists take a different view. They argue that during downturns, governments should step in to boost demand through fiscal measures such as increased public spending or tax cuts. Monetary policy, including lowering interest rates or expanding the money supply, is also seen as a tool to encourage borrowing and investment.

The contrast between these approaches remains a defining feature of modern economic policy debates. In practice, most governments adopt a mix of both perspectives, supporting production while also intervening during periods of economic stress.

Relevance in Today’s Economic Landscape

Say’s Law continues to provide a useful lens for understanding long-term growth. In rapidly developing economies, expanding productive capacity—through infrastructure, education, and technology—often leads to rising incomes and increased consumption.

At the same time, the criticisms of Say’s Law highlight the importance of demand management, especially in the short term. Economic stability depends not only on what an economy can produce but also on whether there is sufficient spending to absorb that production.

The interplay between these two forces—supply and demand—remains central to economic analysis. While Say emphasized production as the starting point, modern economists recognize that both sides of the equation must be considered.

Final Perspective

Say’s Law offers a compelling argument that prosperity begins with production. By focusing on the creation of goods and services, it shifts attention away from money as an end goal and toward the real drivers of economic progress.

Yet, experience has shown that production alone does not always guarantee balanced growth. Economic downturns, financial crises, and shifts in behavior can disrupt the link between supply and demand.

As a result, Say’s Law is best understood not as an absolute rule but as a foundational principle—one that explains how economies function under ideal conditions, while leaving room for other theories to address real-world complexities.

Frequently Asked Questions

Who developed Say’s Law and why does it matter?

The idea was introduced by Jean-Baptiste Say, who wanted to explain how economies grow through production rather than just money circulation.

Why does production create demand?

Because producing something generates wages, profits, and income. That income gives people the ability to spend, which fuels demand for other products.

Does Say’s Law mean money is unimportant?

Not exactly. Money is useful as a tool for exchange, but Say argued it is not the source of wealth—real value comes from production.

How does Say’s Law relate to economic growth?

It suggests that economies grow when they increase output, improve productivity, and expand industries rather than simply encouraging consumption.

What is the circular flow of income in this context?

It’s the idea that firms pay wages to households, households spend money on goods, and that spending becomes revenue for firms—creating a continuous economic cycle.

How does Say’s Law view unemployment?

Classical economists believed persistent unemployment is not caused by lack of demand but by structural issues like skill gaps or wage imbalances.

Why do supply-side economists support Say’s Law?

They believe boosting production—through lower taxes or fewer regulations—leads to higher incomes and naturally increases demand.

What was John Maynard Keynes criticism of Say’s Law?

Keynes argued that demand can fall short of supply, especially during recessions, meaning economies can stagnate without government intervention.

Can Say’s Law fail in real-world situations?

Yes, especially during crises when people save excessively, reduce spending, or lose confidence in the economy.

What role does government play according to Say’s Law?

It generally supports limited intervention, allowing markets to self-correct and letting production drive economic activity.

Is Say’s Law still relevant today?

Yes, it remains influential in modern economics, particularly in debates about growth strategies and policy decisions.