Managing multiple debts in a growing business can become overwhelming. Between juggling repayment schedules, tracking different interest rates, and keeping creditors satisfied, it’s easy to feel like you’re constantly playing catch-up. One strategy that can ease this financial juggling act is business debt consolidation. But how does it work, and is it the right move for your company?

Let’s unpack this concept, examine how it functions, and explore whether it can offer financial relief or clarity for your business.

Understanding the Concept of Business Debt Consolidation

At its core, business debt consolidation means merging several existing debts—such as business credit cards, short-term loans, or merchant advances—into one new loan. This new loan is used to pay off all previous debts, leaving the business with a single monthly payment instead of several.

Why might this be appealing? Simplicity is a big reason. One due date, one lender, and one interest rate can significantly reduce the mental and administrative load. Additionally, if the new loan comes with a lower interest rate or better repayment terms, businesses can save money in the long run.

How the Process Typically Works

Here’s what debt consolidation looks like in real terms: a business approaches a lender and applies for a new loan, specifically intending to use it to pay off current liabilities. The lender will evaluate the business’s financial health, creditworthiness, and repayment history. If approved, the new loan is disbursed, and the business uses the proceeds to eliminate its existing debts.

In some cases, businesses partner with third-party agencies that don’t lend money but manage repayment through debt management programs. These organizations collect a single payment from the business each month and distribute it to various creditors, often negotiating better terms or interest rates on the business’s behalf.

Who Should Think About Consolidating Business Debt?

Not all debt situations are equal, and debt consolidation isn’t a one-size-fits-all solution. That said, some scenarios make a strong case for consolidation:

- If your business is dealing with multiple high-interest debts that are difficult to keep track of.

- If you’ve improved your credit score since the initial loans were taken out.

- If your business cash flow is stable enough to support consistent monthly payments under a consolidated loan.

In these cases, consolidation might not only simplify your financial landscape but also open up new savings opportunities.

Key Benefits of Consolidating Business Debts

The advantages of debt consolidation can be compelling—especially when used responsibly and in the right circumstances.

Easier financial management

Multiple lenders often mean multiple due dates, various interest rates, and inconsistent billing cycles. With consolidation, the administrative burden lightens, freeing up time and mental energy.

Reduced overall cost

If your new loan has a lower interest rate than your combined current debts, you could end up saving significantly. This is especially true if you’re consolidating high-interest credit card balances.

Predictable payments

A single monthly installment makes budgeting more straightforward and predictable, allowing you to plan better and avoid surprise charges or late fees.

Improved credit profile

If consolidation allows you to pay down revolving credit (like cards), your credit utilization ratio could improve—one of the key factors affecting your credit score.

Can Consolidating Business Debt Affect Your Credit?

The short answer is yes, but it’s often temporary. Applying for a consolidation loan usually involves a hard credit inquiry, which might reduce your score slightly. However, this dip is often short-lived.

Over time, consistently paying your new loan on time can improve your credit standing. Moreover, eliminating high-interest debts can make your credit profile more attractive to future lenders.

If your goal is to apply for new funding or expand your business in the near future, consolidation could help present a cleaner and more manageable credit history.

Is Debt Consolidation the Same as a Loan?

While related, the two concepts aren’t interchangeable. A business loan can serve many purposes—buying equipment, hiring staff, or expanding into new markets. Debt consolidation, on the other hand, is a specific use of a loan: to pay off other debts.

Here’s the distinction:

- A business loan is for future-oriented growth or operational needs.

- A consolidation loan is backward-facing, used to restructure or simplify existing debt.

Understanding this difference helps set clearer expectations for how the loan will impact your business finances.

Best Times to Consider Consolidation

Timing matters. Not every stage of business growth or challenge is ideal for consolidation. It may be time to consider this step if:

- You’re buried under several loans or credit cards with different terms and due dates.

- Interest rates on your current debt are eating into your profits.

- You foresee stable income and can commit to fixed payments going forward.

- You want to take advantage of improved credit standing for better lending terms.

Conversely, if your cash flow is inconsistent or you’re on the verge of financial instability, consolidation might not be the right move—at least not yet.

How Many Times Can You Consolidate Business Debt?

Technically, there’s no limit. But practically speaking, frequent consolidation without changing the behaviors that caused the debt in the first place won’t help much. Using consolidation as a bandage instead of fixing underlying problems—like overspending or poor financial planning—can lead you into deeper trouble.

One effective strategy is to treat each round of consolidation as a reset point. Establish better tracking, tighten spending, and create a more robust financial plan moving forward.

Common Pitfalls to Watch Out For

Debt consolidation isn’t without risks. Here are several red flags and mistakes to avoid:

New fees and hidden costs

Some lenders tack on origination, application, or administrative fees that can reduce the savings you hoped to achieve. Always check the fine print.

Extended repayment period

A lower monthly payment might seem like a win, but if the loan term is longer, you may end up paying more interest overall.

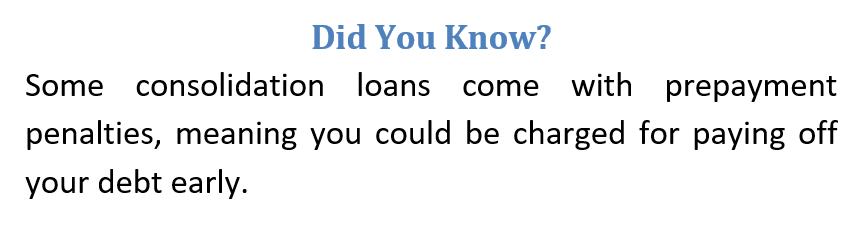

Prepayment penalties

If your plan is to pay off the debt faster than scheduled, ensure your lender doesn’t penalize you for early repayment.

Collateral requirements

If your new loan is secured, be mindful of what you’re putting on the line. Defaulting could mean losing essential business assets.

Consolidation scams

Sadly, not every lender is trustworthy. Watch out for upfront fees, vague terms, or aggressive sales tactics. Stick with lenders that have transparent reputations and established track records.

False sense of security

Having fewer payments doesn’t mean you’ve eliminated the problem. It’s easy to feel relief after consolidating, but continuing to rack up new debt on cleared credit cards will only restart the cycle.

Consolidation Loan Costs: What to Expect

Debt consolidation often comes with various fees depending on the lender and type of loan. These may include:

- Application and origination fees

- Annual fees for business lines of credit

- Collateral valuation or appraisal fees

- Late payment penalties

- Prepayment penalties

- Closing costs

While these costs don’t necessarily make consolidation a bad option, you’ll want to run the numbers to ensure you’re truly saving money.

Qualifications Lenders Look For

If you’re considering a consolidation loan, expect lenders to evaluate you on several key metrics:

Credit score and history

A stronger score generally means better terms and more favorable interest rates.

Financial performance

Stable revenue and profit margins reassure lenders that you can manage consistent repayments.

Collateral availability

Some lenders may require tangible assets to secure the loan.

Debt load and usage

Lenders will assess how much debt you have, how you’ve managed it in the past, and whether consolidation will truly reduce your risk.

If your finances are in rough shape, it might be wise to take a few months to stabilize cash flow or improve credit before applying.

What Are Your Consolidation Options?

There are several ways to consolidate business debt depending on your needs and qualifications.

Term loans

These provide a lump sum repaid over a set period with fixed interest. They’re ideal for paying off specific amounts of debt.

SBA loans

Government-backed and often offering favorable terms, SBA loans are harder to qualify for but can be a great option for well-established businesses.

Alternative lenders

Online platforms or fintech providers offer faster approvals but may come with higher rates.

Business credit cards or balance transfers

Useful for consolidating smaller debts, especially if you qualify for 0% introductory APR offers.

Each option has its pros and cons, so choose one that fits your specific financial landscape.

Is Consolidation the Right Choice for You?

Debt consolidation isn’t a silver bullet. It’s a tool — and like any tool, its effectiveness depends on how you use it.

If you’re determined to clean up your business finances, committed to staying on track, and ready to make smarter financial decisions, consolidation can offer breathing room and long-term savings.

But if it’s used simply to make space for more debt, it may only delay bigger problems. The best way to approach consolidation is with clarity, caution, and a solid plan in place for the future.

Final Words

For many businesses, debt is simply part of the journey. It fuels growth, funds opportunities, and helps bridge cash flow gaps. But when debt spirals out of control, it can become a roadblock.

Business debt consolidation offers a way to streamline and regain control — if done thoughtfully. Before you commit, evaluate your current obligations, review your long-term goals, and ask yourself whether this strategy supports a sustainable future.

Remember, consolidation isn’t just about reducing what you owe — it’s about transforming how you manage your business finances moving forward.

Read Also: Venture Debt Explained: Smart Startup Financing Without Giving Up Equity

FAQS about Business Debt Consolidation

How Can Consolidation Help My Business?

It can reduce financial stress, lower your total interest, improve cash flow, and make budgeting easier by streamlining your payments.

Will My Credit Score Be Affected?

Initially, your score might drop slightly due to a credit inquiry, but it can recover over time with consistent on-time payments and reduced debt balances.

When Should I Consider Consolidating?

If you’re juggling several high-interest debts, have a stable cash flow, or improved your credit score, consolidation might be a smart move.

Are There Any Risks Involved?

Yes. Watch out for hidden fees, extended repayment terms, prepayment penalties, and the temptation to take on new debt after consolidation.

How Do I Know If It’s the Right Choice?

If you’re ready to commit to better financial habits and need a simpler, more affordable repayment plan, consolidation could be a helpful tool—not a cure-all.