In the routine flow of business operations, money does not only move between a company and external parties like customers or suppliers. Quite often, funds shift within the organization itself—for example, when cash is deposited into a bank account or withdrawn for daily use. These internal movements are captured through what accountants call contra entries.

Although they may seem simple at first glance, contra entries play a critical role in maintaining accurate financial records. They ensure that internal fund transfers are properly documented without distorting income, expenses, or overall profitability. To fully appreciate their importance, it is necessary to examine their meaning, structure, purpose, and practical application.

Meaning and Core Concept of Contra Entry

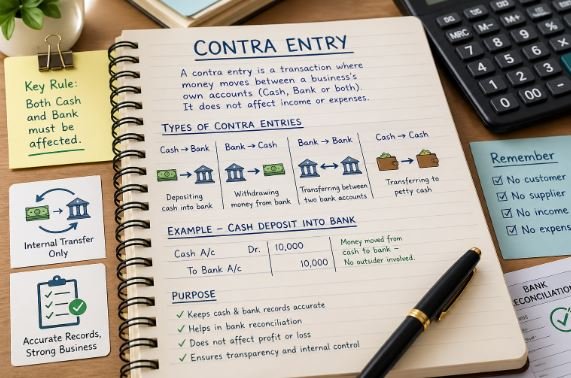

A contra entry refers to a financial transaction that involves the transfer of funds between accounts belonging to the same business. Typically, this movement occurs between cash and bank accounts, though it can also happen between two bank accounts or two cash accounts within the organization.

The defining feature of a contra entry is that it affects two internal accounts simultaneously—one account is debited while the other is credited. However, unlike most accounting transactions, no external party is involved. The funds do not enter or leave the business; they simply change form or location.

In practical terms, this means that when a business deposits cash into its bank account, its cash balance decreases while its bank balance increases by the same amount. The total financial position remains unchanged, but the distribution of funds shifts. This dual effect is what distinguishes contra entries from other types of transactions.

Common Forms of Contra Transactions

Contra entries can take several forms depending on how funds are transferred within the business. The most common scenarios include movements between cash and bank accounts, as well as transfers within similar account types.

One frequent example is depositing physical cash into a bank account. Here, the cash account is reduced, and the bank account is increased. Another typical case involves withdrawing money from the bank for operational use, which increases cash on hand while reducing the bank balance.

Businesses that operate multiple bank accounts may also transfer funds from one account to another. In this case, one bank account decreases while the other increases. Similarly, organizations often maintain a petty cash fund for minor day-to-day expenses. When money is allocated from the main cash reserve to petty cash, it is treated as a transfer between two cash accounts.

Despite their differences, all these transactions share the same underlying principle: they involve internal fund movement without impacting revenue or expenditure.

The Role of Petty Cash in Contra Entries

Petty cash deserves special attention because it introduces a slightly different dimension to contra entries. Many businesses set aside a small amount of money to handle minor expenses such as transportation, office supplies, or quick service payments.

When funds are moved from the main cash account into the petty cash fund, the transaction is still internal. No external payment has been made at that point; the business is simply reallocating its resources. As a result, this movement qualifies as a contra entry.

However, once petty cash is actually spent—for example, on stationery—that subsequent transaction is no longer a contra entry. It becomes an expense because money leaves the business.

Why Contra Entries Are Important

At first glance, recording internal fund transfers might seem unnecessary. After all, the total amount of money remains the same. However, ignoring these transactions can lead to significant inaccuracies in financial records.

One of the primary reasons for recording contra entries is to maintain accurate balances. If a business deposits cash into the bank but fails to record the transaction, the cash book will show funds that are no longer physically available. This creates discrepancies that can complicate financial analysis.

Contra entries also help prevent misclassification of transactions. Without them, internal transfers might be mistakenly recorded as income or expenses, leading to inflated financial figures. Proper classification ensures that financial statements reflect the true performance of the business.

Another important benefit is improved bank reconciliation. By documenting every transfer between cash and bank accounts, businesses can easily match their internal records with bank statements. This process helps identify errors, omissions, or unauthorized transactions.

Additionally, contra entries support transparency during audits. A clear record of all internal fund movements allows auditors to verify the accuracy of financial statements more efficiently.

Illustrative Examples of Contra Entries

To better understand how contra entries function, consider a few practical scenarios.

Suppose a shop owner deposits a portion of daily cash sales into the company’s bank account. In this case, the cash balance decreases while the bank balance increases by the same amount. Since the transaction occurs entirely within the business, it is recorded as a contra entry.

In another scenario, a company withdraws money from its bank account to cover immediate operational needs. Here, the bank balance declines, and the cash balance rises accordingly. Again, no external party is involved, making it a contra entry.

Now compare these with transactions that are not contra entries. If a business pays a supplier using a cheque, the money leaves the organization, so it is recorded as an expense or liability settlement. Similarly, receiving payment from a customer increases the bank balance but represents income, not an internal transfer.

These distinctions are crucial for accurate bookkeeping.

Recording Contra Entries in the Cash Book

Traditionally, contra entries are recorded in a double column cash book, which includes separate columns for cash and bank transactions. This format allows both sides of a contra transaction to be entered within the same book.

Each contra entry appears twice: once on the debit side and once on the credit side. For example, when cash is deposited into the bank, the bank column is debited while the cash column is credited. The reverse occurs when cash is withdrawn from the bank.

To indicate that the transaction is internal and does not require further posting to the ledger, accountants mark it with a “C” in the ledger folio column. This notation serves as a quick reference and prevents duplication of entries.

Modern accounting systems have simplified this process significantly. Software applications automatically update both accounts when a contra entry is recorded, eliminating the need for manual duplication and reducing the risk of errors.

Practical Approach to Recording Contra Entries

In contemporary accounting environments, recording a contra entry typically involves selecting the appropriate voucher type in the accounting system and specifying the accounts involved.

For instance, if funds are transferred from a bank account to cash, the bank account is credited while the cash account is debited. The system then updates both balances simultaneously, ensuring accuracy and consistency.

This automated approach not only saves time but also enhances reliability, especially for businesses that handle a large volume of transactions.

Advantages of Using Contra Entries

Contra entries offer several operational and analytical benefits. One of their main advantages is clarity in financial records. By explicitly documenting internal transfers, businesses can maintain a precise view of how funds are distributed across accounts.

They also streamline the bookkeeping process. Instead of recording separate entries for related transactions, contra entries consolidate them into a single, balanced record. This reduces redundancy and simplifies data management.

Another significant advantage is their role in bank reconciliation. Since all transfers between cash and bank accounts are clearly recorded, matching internal records with bank statements becomes more straightforward.

From an audit perspective, contra entries provide a transparent trail of fund movements. This transparency enhances credibility and facilitates compliance with financial reporting standards.

Finally, because contra entries do not affect income or expenses, they preserve the integrity of profit calculations while still capturing essential financial activity.

Limitations and Challenges

Despite their usefulness, contra entries are not without challenges. One potential issue is the complexity they introduce, particularly in manual accounting systems. Recording both sides of each transaction requires attention to detail, and errors can lead to imbalances.

There is also a risk of misinterpretation, especially among individuals who are not well-versed in accounting principles. Incorrect classification of transactions can distort financial records and create confusion.

In some cases, combining multiple internal transfers into a single entry may reduce visibility into individual transactions. This can limit detailed analysis if not managed carefully.

Moreover, accurate documentation is essential. Missing or incomplete records can complicate reconciliation and auditing processes, making it harder to verify financial data.

Common Errors to Avoid

One of the most frequent mistakes in accounting is misidentifying transactions as contra entries. A key rule to remember is that both accounts involved must belong to the business, and the transaction must not involve any external party.

For example, withdrawing money from the business for personal use is not a contra entry. Such transactions are classified as drawings and are recorded separately under the owner’s capital account.

Similarly, payments to suppliers or receipts from customers should never be treated as contra entries, as they represent external financial interactions.

Understanding these distinctions is essential for maintaining accurate and reliable records.

Final Thoughts

Contra entries may appear routine, but they are fundamental to effective financial management. By capturing internal fund movements accurately, they help maintain consistency, prevent misstatements, and support essential processes like reconciliation and auditing.

Whether handled manually through traditional cash books or automatically via accounting software, the underlying principle remains the same: every internal transfer must be recorded in a way that reflects both sides of the transaction.

For businesses of all sizes, mastering contra entries is a practical step toward stronger financial control and more reliable reporting.

Frequently Asked Questions about Contra Entry

Why are contra entries recorded if no money leaves the business?

They are recorded to keep financial records accurate. Without them, cash and bank balances would be misleading, making it difficult to track actual funds.

Which accounts are involved in a contra entry?

Contra entries usually involve cash accounts, bank accounts, or both. In some cases, they may also include petty cash accounts within the business.

Does a contra entry affect profit or loss?

No, it does not impact profit or loss because it only involves internal movement of funds. The total financial position remains unchanged.

What are common examples of contra entries?

Typical examples include depositing cash into a bank, withdrawing cash for office use, transferring funds between bank accounts, and allocating money to petty cash.

How can you identify a contra entry quickly?

A transaction is a contra entry if it affects both cash and bank accounts (or similar internal accounts) and does not involve any external party.

What is the role of petty cash in contra entries?

Petty cash is used for small daily expenses. Transferring funds into petty cash from the main account is considered a contra entry because it’s an internal allocation.

How are contra entries recorded in traditional bookkeeping?

They are recorded in a double column cash book, appearing on both debit and credit sides, often marked with a “C” to indicate a contra transaction.

Are contra entries still relevant with modern accounting software?

Yes, but software automates the process. Once recorded, both accounts update instantly, reducing manual effort and errors.

What is the biggest mistake to avoid with contra entries?

A common mistake is treating personal withdrawals or payments to suppliers as contra entries. These involve external parties and should be recorded differently.

How do contra entries help in bank reconciliation?

They make it easier to match internal records with bank statements by clearly documenting all transfers between cash and bank accounts.